|

Report from

Europe

Rising demand and limited supply push plywood

prices

Plywood prices are rising sharply in the EU on the back of

buoyant demand across the region and supply issues in a

range of key exporting countries.

There is also now an increasing tendency to order more

just-in-time, little and often to hedge against the risk of the

present ˇ®market bubbleˇŻ bursting.

That summarises recent feedback from leading European

plywood importers and distributors on trade and market

trends.

One leading player described market dynamics over the

last six months as ˇ®increasingly trickyˇŻ. It had reached the

point where, due to constrained supply and competition for

what supply there was, the company was now effectively

rationing product.

ˇ°ThereˇŻs certainly no need for advertising currently ¨C

everything weˇŻre bringing in is already sold,ˇ± he said. ˇ°In

fact, weˇŻre allocating product to a waiting list, with loyal,

long-term customers obviously at the front of the queue.ˇ±

Adding to market challenges, importers say they have had

to become ever more selective in choice of supplier in

response to what they describe as increasingly stringent

and more uniform application of the EU Timber

Regulation (EUTR).

ˇ°This and our own increasingly strict corporate social

responsibility policy and stress on minimising reputational

risk means that, where we previously had 10-15 suppliers,

we now have just four or five who we know we can rely

on to consistently satisfy our due diligence requirements,ˇ±

said another importer. But clearly that potentially

exacerbates availability issues when supply is tight

generally.

Descriptions of price rises resulting from this combination

of market pressures range from ˇ®significantˇŻ to ˇ®seismicˇŻ.

A UK importer said in the last six months theyˇŻve seen

prices for Malaysian and Chinese tropical plywood

increase 25% and 20% respectively, while Brazilian

elliottii is up 30%.

A continental European buyer said theyˇŻd seen an even

steeper hike in the cost of elliottii pine plywood since last

June. ˇ°Then we were paying US$240/245 per cu.m fob for

standard 20mm C+C, now weˇŻre at US$330,ˇ± they said.

ˇ°WeˇŻve been cushioned to an extent by the weakening of

the dollar, which nine months ago was at euro1.06 and is

now euro1.23. But even so, a rise of US$80 per cubic

meter is a lot to take on board ¨C and if the dollar

strengthens, weˇŻll be in for even stiffer rises. Larger

customers with a more global perspective understand the

situation and accept they have to pay more, but efforts to

pass on at least some of the increases to smaller businesses

are meeting with resistance.ˇ±

The main driver for EU demand of both tropical and

temperate hardwood and coniferous plywood is continuing

construction growth across much of the EU, particularly,

according to one international importer/trader, in north

west European countries where a relatively mild winter

has meant the market has remained more active than usual

at this time of year.

The latest report from Euroconstruct forecast 2017

construction growth in its 19 focus countries at 3.5%. It

added that it was the first time there had been an ˇ®across

the boardˇŻ increase in activity in all countries since 1989,

and that growth in a basket of construction market

measures was at its highest since 2006.

The result, say suppliers is healthy demand for everything

from shuttering/formwork plywood, to top end structural

and exterior grades.

Furthermore, Euroconstruct predicts that the EU building

sector will see another 6% expansion by 2020, with civil

engineering projects and refurbishment and maintenance

sectors taking over from residential and non-residential

building in providing most market momentum.

But - Risk of overheating plywood market

For the immediate future, the EU plywood sector sees

little change in trading conditions. Further ahead,

however, the picture is less certain. ˇ°There are now signs

of the market overheating, and at some point there will be

a correction,ˇ± said an importer distributor.

ˇ°I donˇŻt see it in the next six months but, if US buyers exit

the Brazilian market, as weˇŻve seen happen before, our

other leading global suppliers raise output and demand

comes off current levels, we could be looking at a very

different market scenario from the fall onwards. Leading

up to this point I think weˇŻre already seeing more cautious,

hand to mouth purchasing so companies arenˇŻt overexposed.ˇ±

Buoyant EU economy

EU building growth is underpinned by generally buoyant

economic performance and this, in turn, says the plywood

sector, is fuelling sales rises in other markets, notably

packaging and furniture.

Demand in the latter is reported being given added

impetus by a design trend to use plywood as the sole

manufacturing material, with faces and edges expressed,

even unfinished, to reveal its structure and achieve an

ˇ®industrial lookˇŻ. Birch is the favoured species here, but

one leading kitchen maker said they were also exploring

the use of darker-faced tropical varieties.

Against this bullish economic backdrop, latest EU

plywood import statistics make clear why the market

generally is reporting a squeeze on supply. Imports didnˇŻt

just fail to keep up with demand last year, they declined.

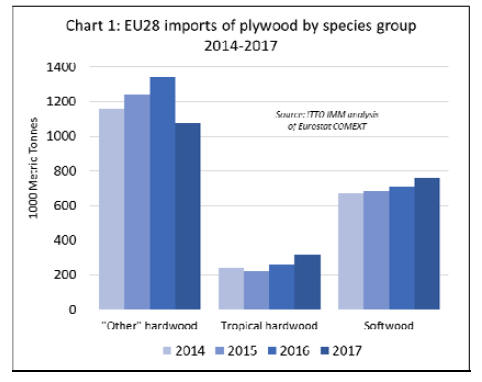

EU plywood imports down 7% in 2017

Total EU plywood imports in 2017 were down 7% to

2.159 million metric tonnes (MT). This was due entirely to

contraction in the ˇ®other hardwoodˇŻ plywood category,

with imports down over 20% from 1.346 million MT to

1.076 million MT.

Part of this was likely due to a revision of customs product

codes in 2017, which saw a large number of species

previously labelled ˇ®other hardwoodsˇŻ now identified as

ˇ®tropicalˇŻ.

However, this was clearly not the only factor in the

downturn, as tropical and softwood plywood imports

increased by a combined total of only 115,000 MT in

2017; the former rising from 262,000 MT to 320,000 MT,

the latter from 707,000 MT to 760,000 MT. (Chart 1)

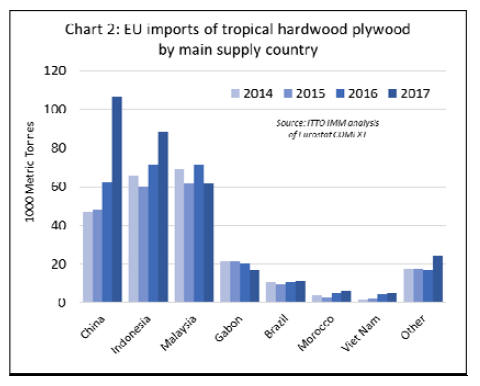

Overtaking both Indonesia and Malaysia as the largest

supplier of tropical hardwood to the EU was China, with

imports up 44,000 MT to 106,000 MT in 2017. This is

almost entirely due to the HS product code

reclassification, as Chinese ˇ®mixed red hardwoodˇŻ

plywood was most affected.

EU imports of Indonesian plywood were ahead 24% in

2017, rising from 71,000 MT to 88,000 MT, while imports

of Malaysian plywood dipped 15% from 71,000 MT to

62,000 MT, and imports of Gabon plywood fell 19% from

21,000 MT to 17,000 MT. (Chart 2).

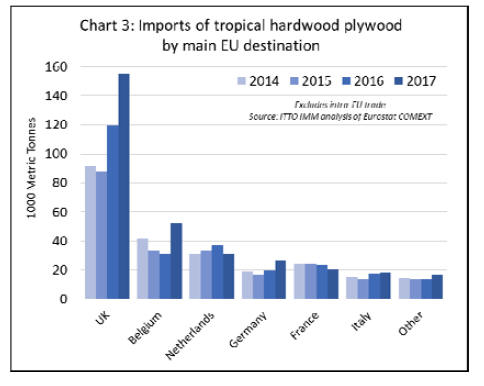

The largest EU tropical plywood importer in 2017

remained the UK, which increased its purchases by 29%

from 120,000 MT to 155,000 MT.

Belgium became the second biggest, with imports rising

21,000 MT to 52,000 MT, taking over from the

Netherlands where imports fell 6,000 MT to 31,000 MT.

Germany also saw an increase of 35% to 27,000 MT in

2017. (Chart 3).

FLEGT licensing and plywood demand

The extent to which the start of FLEGT licensing in

November 2016 played a part in IndonesiaˇŻs EU export

growth last year is a matter of debate, but the consensus

amongst importers seems to be that it was one of several

factors and it is now becoming more important.

One importer said the availability of third-party quality

assured marine plywood from Indonesian producers was

more of a factor in their increased imports. But another

said they had ˇ°switched sourcing to Indonesia to a degreeˇ±

due to the availability of FLEGT licensed material and the

savings in administrative time and cost on EUTR due

diligence involved.

Meanwhile, a Belgian importer distributor saw a FLEGT

licence becoming an increasingly valuable reputational

guarantee. He suggested that EUTR monitoring and

enforcement activity are growing, led by the national

competent authorities (CAs) of Germany, the UK,

Netherlands and Denmark, and to a degree France, and

with others just beginning to step up capacity to undertake

more checks, including in Belgium.

This importer also suggested that thereˇŻs now greater

operational collaboration and intelligence sharing between

CAs. ˇ°ItˇŻs got to the point where companies like ours are

adopting a zero-tolerance policy on risk of any illegal

material entering our supply chain. If we have any doubts

about a supplier, species or source of supply, we wonˇŻt use

themˇ±, he said.

He went on, ˇ°in that context a product backed by a

FLEGT licence as proof of legality clearly is set to

become an increasingly attractive option.ˇ±

Multiple plywood supply constraints

EU plywood importers suggest that recent trends in

imports have been driven as much by supply side issues as

by changes in European consumption. Supply constraints

have been mounting in the last six months.

According to one importer, the severe rainy season in

Indonesia was an important factor limiting supply of

tropical hardwood plywood last year. Harvesting was

impacted and mills were running increasingly short of raw

material.

ˇ°Indonesia may have increased its exports to the EU

overall last year, but more recently weˇŻve been getting as

little as 50% of normal deliveries,ˇ± said the company.

ˇ°Many mills must be losing money and some have gone

on to short-time, or mothballed production.ˇ±

This importer was hoping that the rainy season will finish,

as normal, end of March. ˇ°But last year that didnˇŻt

happen,ˇ± said another importer. ˇ°Some feel itˇŻs another

possible sign of climate change. It maybe weˇŻre facing

more unpredictable weather patterns generally and our

industry will just have to adapt.ˇ±

Chinese environmental regulation reduces plywood

supply

EU plywood importers also report that production output

of their Chinese suppliers is being affected by tough new

environmental and health and safety regulations. This has

forced Chinese producers to invest heavily in new

production and pollution control technology. Some have

cut or even stopped production while installation work

goes on.

ˇ°The new rules are also driving many of the small-scale,

family-run, rotary cut veneer plywood manufacturers out

of business,ˇ± said an importer. ˇ°They principally served

the domestic market, so now domestic customers are also

turning to the bigger export producers, adding another

supply pressure.ˇ±

Chinese producers looking for higher prices

ItˇŻs generally agreed that the main pressure on elliottii

supply has been rising global demand. Brazilian mills last

year were reported to have topped 2 million cubic metres

in output last year, but EU importers say their US

counterparts have been buying particularly heavily, and

demand elsewhere in the region has also risen, including

in Mexico and Caribbean markets.

ˇ°Add in freight rate rises, and thatˇŻs why elliottii has

become an increasingly costly commodity,ˇ± said one EU

importer.

Weather is cited as a factor in recent Russian supply

trends. A slow start to the winter, is reported to have

delayed harvesting, leading to a backlog of orders. ˇ°Now

mills are sold quite well ahead, with order books full for

March and April,ˇ± said an EU importer. ˇ°We anticipate a

price uptick as a result.ˇ±

EU associations push for higher plywood quality

standards

Timber trade associations in two leading EU importing

countries have recently been pushing forward plywood

quality, performance and legality initiatives.

In the UK, the Timber Trade Federation (TTF) has

undertaken a Plywood Review over the last 18 months.

This is in response to concerns over import of products,

mainly from China, that the TTF claims do not meet key

EU/UK legal compliance legislation.

That included products classified as high risk under the

EUTR not being adequately risk mitigated through tropical

veneer species testing. The initiative was also in response

to insufficient glue-bond testing being undertaken, notably

in EN.314 Class 2 product, to be able to draw up a

Declaration of Performance (DoP).

The TTF has liaised with Chinese trade associations on

these issues and produced recommendations for members.

These include; for EUTR compliance, to implement

regular plywood species testing from high-risk suppliers;

to provide clear species marking on packs; and to ensure

suppliers operate documented Factory Production Control

(FPC) in compliance with the EU Construction Products

Regulation.

The TTF said the review is ongoing and will be subject to

more discussion and actions in coming weeks.

In Germany, GD Holz has been continuing to develop its

Plywood Quality Initiative (Initiative Qualitäts Sperrholz

/IQS). With five member importers, and aims to include

more, the focus is on ˇ®ensuring correct description of all

product characteristics and propertiesˇŻ.

The companies are obliged to ensure suppliers meet

national product codes and to include all relevant product

technical details and descriptions with deliveries.

Recently GD Holz has issued a leaflet to inform membersˇŻ

customers what to expect from an IQS supplier and a

brochure detailing softwood and hardwood plywood

production codes of Brazil (ABNT), Russia (GOST),

Finland (SFS) and the EU (DIN-EN).

Currently IQS is concentrated on technical issues, but it

intends eventually to add legality and sustainability to its

remit.

|