|

Report from

Europe

Recovery in EU wood imports continues in 2018

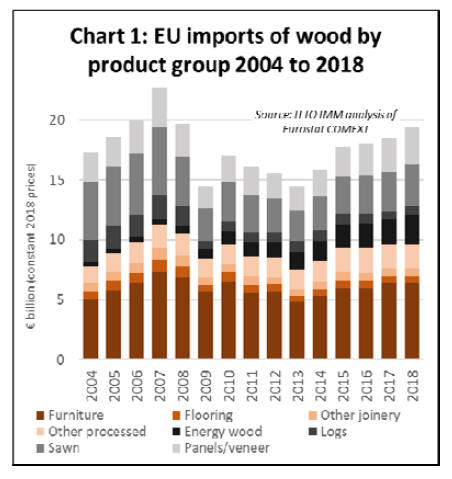

The total value of EU imports of wood products was 19.44

billion euro in 2018, 5.1% more than in 2017. This

followed an increase of 2.4% to 18.49 billion euro in 2017.

In 2018 EU import value was at the highest level since

2008 just before the global financial crises (Chart 1).

The rise in imports into the EU occurred despite slowing

economic growth during 2018. According to the EU

Winter 2019 Economic Forecast published on 7 February,

economic activity in the EU moderated in the second half

of last year as global trade growth slowed, uncertainty

sapped confidence and output in some Member States was

adversely affected by temporary domestic factors,

including social tensions and uncertainty over fiscal policy

and Brexit.

As a result, GDP growth in both the euro area and the EU

likely slipped to 1.9% in 2018, down from 2.4% in 2017.

Slowing economic growth fed through into a fall in the

value of the euro and the British pound last year, both of

which weakened against the U.S. dollar by around 8%

during 2018. However, EU currencies remained strong

relative to currencies in several key Eastern European

supply countries, including Ukraine, Russia, and Turkey.

Both the euro and British pound strengthened by around

7% against the Russian rouble in 2018 and by over 25%

against the Turkish lira. These exchange rate fluctuations

generally favored EU imports from Eastern Europe and

acted as a drag on imports from North America and Asia.

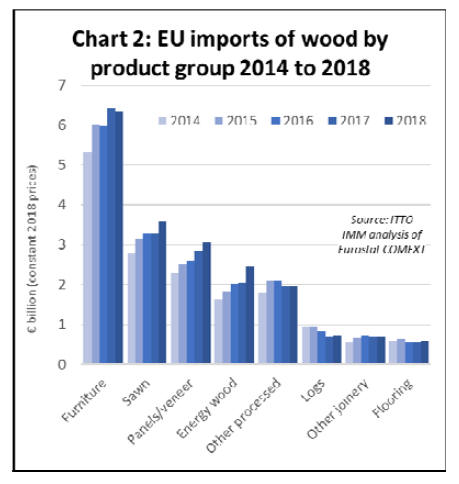

Considering individual products (Chart 2), the value of EU

imports of wood furniture decreased by 1% to 6.35 billion

euro in 2018 after a 7% rise in 2017. A dip in EU imports

of wood furniture from China and Norway was offset by

rising imports from Ukraine, Belarus, Bosnia, Serbia,

Russia and Turkey.

This forms part of general trend of increasing EU

dependence on wood furniture manufactured in central and

Eastern Europe. EU wood furniture imports from tropical

countries, led by Vietnam, Indonesia and Malaysia, were

flat overall last year, although imports from India

continued to rise.

Growth in EU imports of sawn wood resumed in 2018

after flat-lining the previous year. The total value of EU

imports of sawnwood (including both softwood and

hardwood) in 2018 was 3.59 billion euro, nearly 10%

more than in 2017.

There was a particularly significant 21% increase in the

value of EU sawnwood imports from the CIS countries in

2018, building on an 11% increase the previous year. Most

of the increase in sawnwood imports from CIS countries in

2018 came from Ukraine, Belarus and Russia and is due

both to currency weakness and increasing controls on log

exports from these countries.

EU imports of sawnwood, both softwood and hardwood,

increased sharply from Brazil in 2018. Imports of tropical

sawn wood from both South East Asia (most notably from

Malaysia and Myanmar) and Africa (mainly Cameroon,

Gabon and Congo) regained some ground in 2018 after a

sharp fall the previous year. EU imports of sawnwood

from North America slowed a little in 2018.

EU imports of panels (mainly plywood) increased 8% to

Euro 3.06 billion in 2018. This follows a 9% rise in 2017

and is the fifth consecutive year of import growth of this

commodity.

As for other wood commodities, much of the gain was due

to a rise in plywood imports from Russia, Ukraine and

Belarus, however plywood imports from China, Brazil and

Indonesia also increased in 2018.

Imports of plywood and veneer from Gabon slowed in

2018, being affected by the financial problems of the

Rougier group. There was a partial recovery in veneer

imports from Cote dˇŻIvoire in 2018. EU imports of

composite panels increased from Turkey.

The long-term rise in EU imports of energy wood

accelerated in 2018 with annual import value rising over

20% to 2.47 billion euro. This followed a slowdown to

only 3% growth in 2017 after average annual growth of

11% in the previous five years.

There was another sharp increase in EU imports of energy

wood from the United States in 2018 (now dominated by

pellets), to reach over 1 billion euro for the first time, with

most destined for the UK. Imports of energy wood also

increased sharply from Russia, Belarus and Ukraine,

mainly destined for continental EU. Import growth also

resumed from Brazil and Uruguay.

EU imports of other joinery products (mainly doors and

laminated wood for window frames and kitchen tops)

increased 1% to Euro 710 million in 2018, recovering

from a 1% fall the previous year.

Imports of joinery products from Russia, Ukraine and

Belarus continued to rise last year, with gains also made

by Indonesia, Vietnam, Bosnia, and Turkey.

China continued to lose ground, although it maintained its

position as the single largest external supplier of this

commodity group in the EU market, just ahead of

Indonesia. EU imports of joinery products were stable

from Malaysia in 2018.

After falling back 9% in 2016 and staying flat in 2017, EU

imports of wood flooring increased 2.6% to 580 million in

2018.

Flooring imports from China, by far the largest external

supplier accounting for around two thirds of the total,

recovered ground in 2018, while imports from Ukraine

increased sharply, helping to offset a decline in imports

from Indonesia, Malaysia, Brazil and Switzerland.

Pace of decline in EU tropical timber imports slows

The total value of EU imports of tropical timber products

(including direct imports and imports via third countries

such as China) increased 1.7% to 4.05 billion euro in

2018. This follows a 0.4% fall in import value in 2017.

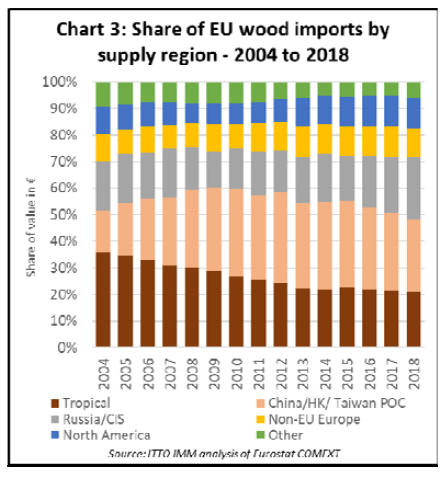

The share of tropical timber in the total value of EU wood

product imports declined from 21.5% in 2017 to 20.8% in

2018. Although 2018 was the third straight year of

declining share for tropical timber, the rate of decline is

now much slower than in the decade prior to 2014 when

share fell continuously from around 36% to 22% (Chart

3).

ChinaˇŻs share in total EU imports of timber products fell

from 29.4% in 2017 to 27.2% last year, the lowest level

since 2007. Meanwhile the share of Russia and other CIS

countries increased from 21.0% to 23.9%. In 2018, there

was a slight decrease in share of EU imports from non-EU

European countries (from 11.1% to 10.6%) and North

America (from 11.7% to 11.6%).

The slight increase in the total value of EU wood product

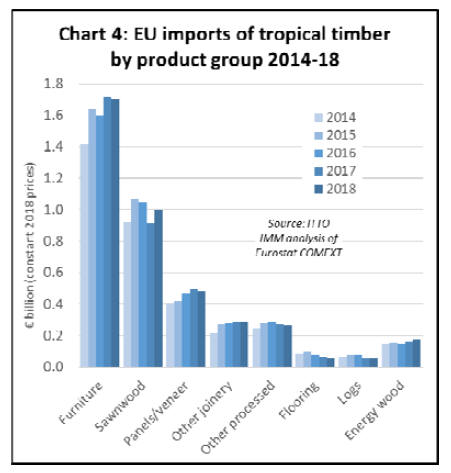

imports from the tropics in 2018 hides variations between

products groups (Chart 4). In 2018, there was a 9%

increase in EU imports of tropical sawn wood, from 914

million euro to 996 million euro, a rebound following the

13% decline the previous year.

There was also an increase in imports of energy wood

from tropical countries, rising from 160 million euro in

2017 to 179 million euro in 2018, with the biggest gains

comprising charcoal from Nigeria and other forms of

fuelwood from Congo and CAR.

The value of EU imports of other tropical products ¨C

including furniture, joinery, plywood, veneers, and logs -

were either flat or declining in 2018. The decline in

imports of tropical flooring was particularly dramatic,

down 15% to 59 million euro in 2018, following on from

an average decline of around 15% in each of the previous

three years.

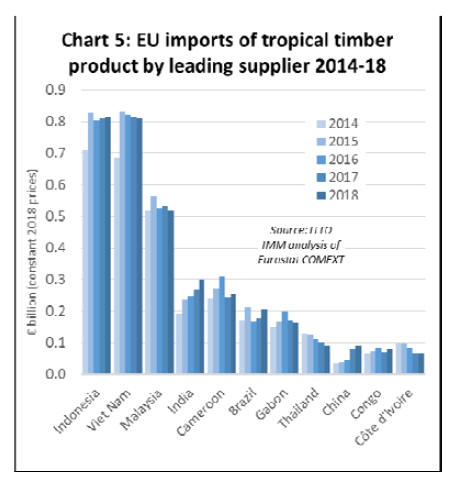

The value of EU imports of all wood products from the

two leading tropical suppliers, Indonesia (813 million

euro) and Vietnam (812 million euro) was stable in 2018.

Total import value declined from Malaysia (by 5% to 519

million euro), Gabon (by 5% to 163 million euro) and

Thailand (by 13% to 90 million euro). (Chart 5)

However, these declines were offset by rising imports

from India (by 12% to 299 million euro, mainly furniture),

Brazil (by 16% to 205 million euro, mainly hardwood

sawnwood and decking), and China (by 15% to 89 million

euro, mainly tropical faced plywood). There was also

recovery in imports from some African countries, mainly

of sawn wood, including Cameroon, by 4% to 252 million

euro, and Congo, by 12% to 79 million euro.

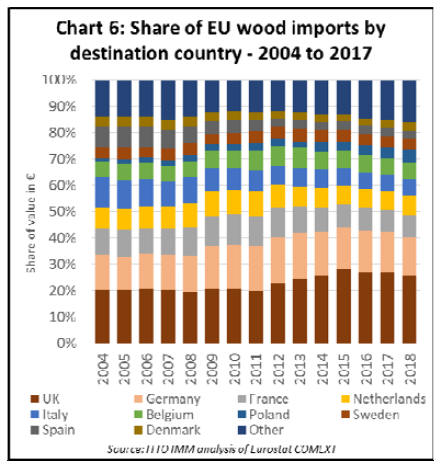

Shifting destinations for EU timber imports

There are significant shifts on-going in destinations for EU

imports of timber products. After emerging as by the

largest single market in the EU for timber products from

outside the bloc between 2011 and 2015, the relative

importance of the UK eased a little in the 2016 to 2018

period.

The UKˇŻs share of total EU imports of timber products

from outside the region declined from a peak of 27.6% in

2015 to 25.0% in 2018. (Chart 6).

The UKˇŻs emergence as the leading EU market for

external timber suppliers between 2011 and 2015

coincided with relatively strong economic growth in the

country and rising consumer demand. This drove a strong

increase in imports from outside the EU, particularly wood

furniture and plywood from China, and wood furniture

from Vietnam.

There was also a big increase in UK imports of wood

pellets, mainly from the U.S., driven by the UKˇŻs climate

change commitments which encouraged some large

energy suppliers to switch from coal to biomass.

However, between 2016 and 2018, growth in the UK

economy slowed, particularly with rising uncertainty over

the effects of Brexit, currently scheduled for 29 March

2019 (but may be delayed for at least a few months,

although nobody yet knows for sure). The British pound

also weakened significantly on foreign exchange markets

during this period, dampening import growth.

Against this background, the fact that the Euro value of

UK imports from outside the EU remained flat at around

4.9 billion euro between 2016 and 2018 is a positive

outcome. During the same period, imports from outside

the EU by most other western European countries also

remained quite flat (Chart 7).

The Netherlands is an exception, experiencing strong

import growth, rising consistently from a low of 1.03

billion euro in 2013 to 1.42 billion euro last year on the

back of economic recovery and rising construction activity

in the country. The Netherlands is also playing a larger

role as a gateway for imports for distribution throughout

the EU.

In 2018, there was also a significant recovery in the value

of imports of timber products from outside the EU by two

countries that formerly were leading players in the global

timber trade but have since waned in significance; France

(up 8% to 1.62 billion euro), and Italy (up 8% to 1.17

billion euro).

In the case of France, imports increased sharply from

China (notably in furniture) in 2018, with gains also made

in imports from Vietnam (furniture), Brazil (hardwood

decking), and Russia (sawn softwood). For Italy, imports

in 2018 increased from Russia (mainly plywood), Ukraine

(mainly sawnwood), Bosnia (mainly energy wood), Brazil

(softwood plywood), Cameroon (sawnwood) and

Myanmar (sawnwood).

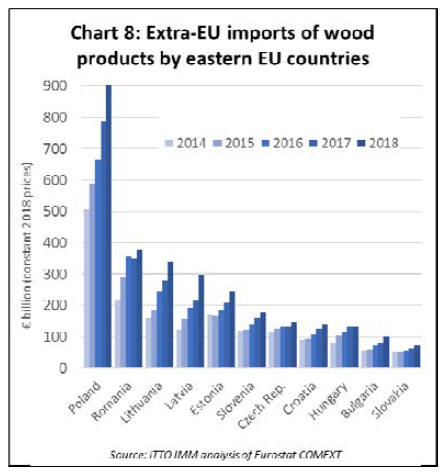

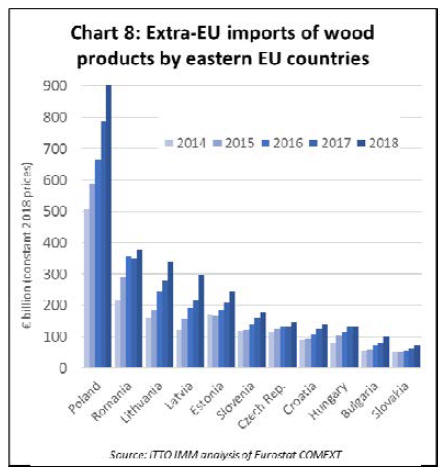

Rising share of EU timber imports destined for Eastern

Europe

While there was some increase in imports by a few

western European countries in 2018, eastern EU countries

recorded much larger and more consistent gains in imports

from non-EU countries last year. Large increases were

recorded in Poland, Romania, Lithuania, Latvia, Estonia,

Slovenia, Czech Republic, Croatia, Hungary, Bulgaria,

and Slovakia (Chart 8).

This is a reflection both of their proximity to Russia,

Ukraine and Belarus, the source of most of the rising

imports, relatively higher rates of economic growth and

construction sector growth in Eastern Europe, and the

establishment of new wood processing and manufacturing

capacity in the region.

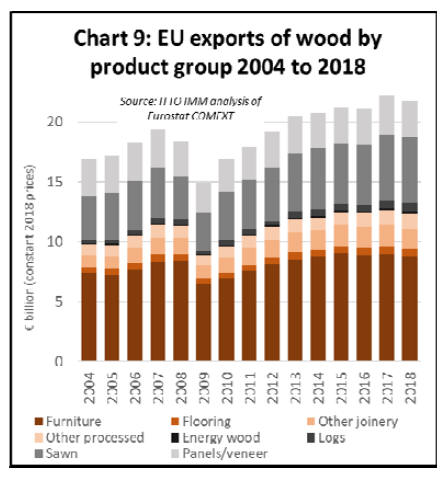

EU wood products exports at record level in 2018

In 2018, the EU exported wood products with a total value

of 21.8 billion euro, 2% less than in 2017 when exports

were at record levels (Chart 9). EU exports of wood

furniture, flooring and other joinery products, and

plywood and other panels all slowed last year, a response

to general cooling in the global economy.

However, EU exports of logs and sawnwood continued to

increase in 2018 to record levels for these commodities,

exports of sawnwood up 2% to 5.54 billion euro and

exports of logs rising by over 14% to 735 million euro.

In 2018, the value of EU timber product exports continued

to rise to the USA but was flat or declining to the other

leading export markets including Switzerland, Norway,

China, Japan, Russia, Egypt and Algeria.

The combined effect of last yearˇŻs fall in EU export value

and rise in EU import value was to reduce the EUˇŻs trade

surplus in timber products with the rest of the world from

3.70 billion euro in 2017 to 2.38 billion euro in 2018.

|