|

Report from

Europe

EU27 tropical wood product imports

close to decade

high in March

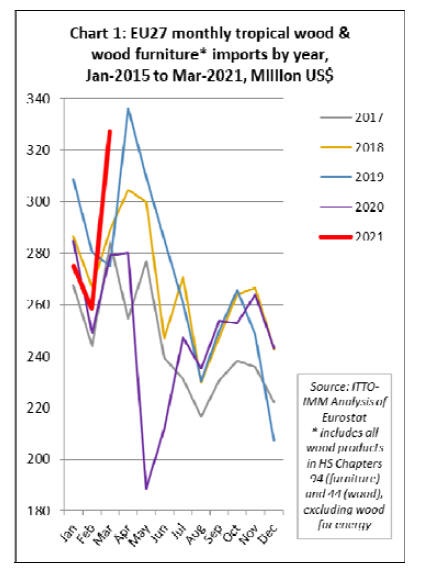

EU27 import value of tropical wood and wood furniture

products was US$861 million in the first three months of

this year, 6% more than the same period in 2020.

After a slow start to the year in January and February,

imports surged to US$327 million in March, only the

second time since 2012 that monthly imports have

exceeded US$325 million (the only other occurrence being

in April 2019) (Chart 1).

The high level of EU27 tropical wood product imports in

March came at a time when most of the continent was still

subject to tight lockdown conditions and probably partly

reflects a surge in deliveries delayed in previous months

due to shortages of containers and other logistical

problems.

However, there also encouraging signs that the economic

recovery in the EU is gaining momentum, a trend expected

to continue as vaccination rates are rising, lockdown

measures are eased and the full effects of

NextGenerationEU, the EUˇŻs large fiscal stimulus

programme, begin to be felt.

EU27 economic forecast revised upwards

According to the EUˇŻs Spring 2021 Economic Forecast

published on 12 May, following a 6.1% decline in 2020,

the EU economy will expand by 4.2% in 2021 and by

4.4% in 2022. This represents a significant upgrade of the

growth outlook compared to the Winter 2021 Economic

Forecast which the Commission presented in February.

Growth rates will continue to vary across the EU, but all

Member States should see their economies return to precrisis

levels by the end of 2022.

The Forecast notes that the rebound in Europe's economy

that began last summer stalled in the fourth quarter of

2020 and in the first quarter of 2021, as fresh public health

measures were introduced to contain the rise in the number

of COVID-19 cases. However, the rise in vaccination rates

and easing of lockdown restrictions is expected to drive a

strong rebound in private consumption and investment.

Growth is expected to be bolstered by rising demand for

EU exports from a strengthening global economy. Public

investment, as a proportion of GDP, is also set to reach its

highest level in more than a decade in 2022 driven by the

Recovery and Resilience Facility (RRF), the key

instrument at the heart of NextGenerationEU.

While the outlook is more positive, the Forecast

emphasises that the risks are high and will remain so as

long as the shadow of the COVID-19 pandemic hangs

over the economy. Developments in the epidemiological

situation and the efficiency and effectiveness of

vaccination programmes could turn out better or worse

than assumed in the central scenario of this forecast.

The forecast may underestimate the propensity of

households to spend or it may underestimate consumers'

desire to maintain high levels of precautionary savings.

The impact of corporate distress on the labour market and

the financial sector could yet prove worse than anticipated.

Forward looking indicators show that economic

momentum in the EU27 has picked up since the start of

the year, although business and consumer confidence is

still quite fragile, particularly in the construction sector, a

key driver of timber demand in the region.

The EUˇŻs consumer confidence indicator reached its

highest level in one year in March, pushing the quarterly

average up to -14.8, 1.9 points above the previous quarter.

The EUˇŻs Economic Sentiment Indicator (ESI) continued

to recover, edging up to 109.7 in April 2021, markedly

above its long-term average and higher than its prepandemic

level for the first time since the outbreak of

COVID-19 on the continent.

ˇˇ

Similarly, MarkitˇŻs Flash Purchasing ManagersˇŻ

Composite Output Index for the euro area stayed above its

no change mark of 50 for a second month in a row in

April, after four months of decline. It was up by 0.5 points

to 53.7.

The IHS Markit Eurozone Construction Total Activity

Index was unchanged at 50.1 in April, signalling only a

fractional expansion in euro area construction activity for

the second successive month. Construction firms often

linked the slight expansion to a resumption of work on

paused projects and were increasingly concerned about the

impact that renewed COVID-19 restrictions have had on

overall demand in the construction sector.

According to IHS Markit, work undertaken on housing by

euro area construction firms increased for a second

successive month in April. The rate of growth quickened

from March and was the strongest recorded since February

2020.

A renewed contraction in home building activity in

Germany was offset by a survey record expansion among

Italian housebuilders. French firms, meanwhile, reported

stable conditions in housebuilding for the second month in

a row.

Commercial construction activity contracted again in the

latest HIS Markit survey period, extending the current

sequence of decline to 14 months. That said, the pace of

the reduction eased from March and was the softest in the

sequence.

A softer fall in commercial activity in France and a

stronger rise in Italy contributed to the easing in the rate of

decline. However, firms in Germany signalled a further,

marked decline in commercial building. The downturn in

euro area civil engineering activity continued in April, as

work undertaken on infrastructure projects contracted at a

modest pace.

The IHS Markit survey shows that the degree of optimism

regarding the outlook for construction activity over the

coming 12 months eased in April and was the softest

recorded for three months. German constructors signalled

renewed pessimism regarding the year ahead outlook, with

projections at their weakest since December 2020.

French firms indicated a lower level of positive sentiment,

though Italian firms signalled the strongest projections

since August 2001.

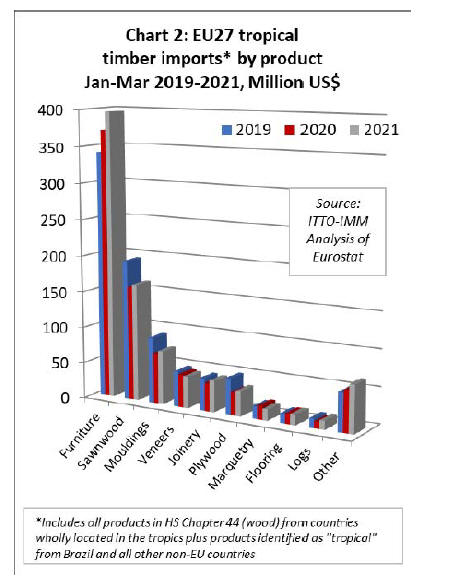

Rebound in EU27 tropical wood product imports in

first quarter

The value of EU27 imports of most tropical wood

products increased in the first three months of 2021

compared to the same period in 2020. This is encouraging

given that Europe only began to lockdown in the middle of

March last year, too late to significantly impact on trade

volumes in the first quarter of 2020.

EU27 imports of wood furniture from tropical countries

increased 7% to US$396 million in the first quarter this

year compared to the same period in 2020, while imports

of tropical sawnwood increased 3% to US$163 million,

tropical mouldings were up 6% to US$74 million, joinery

up 11% to US$43 million, plywood up 10% to US$34

million, flooring up 3% to US$15 million, and logs up

27% to US$12 million.

These gains offset a 4% decline in veneer imports to

US$44 million, and a 17% fall in marquetry imports to

US$16 million (Chart 2).

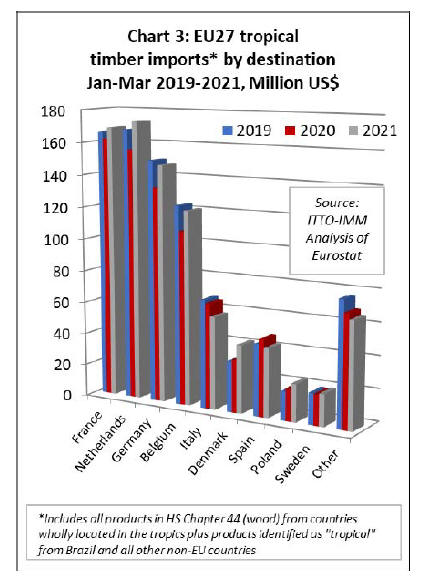

In the first quarter this year, import value increased into all

the largest EU27 destinations for tropical wood and wood

furniture products with the exception of Italy and Spain.

Import value was up 4% to US$169 million in France,

11% in the Netherlands to US$173 million, 11% in

Germany to US$147 million, 12% in Belgium to US$120

million, 30% in Denmark to US$42 million, 17% in

Poland to US$23 million, and 4% to Sweden to US$20

million. Import value decreased in Italy by 12% to US$58

million and by 11% in Spain to US$42 million (Chart 3).

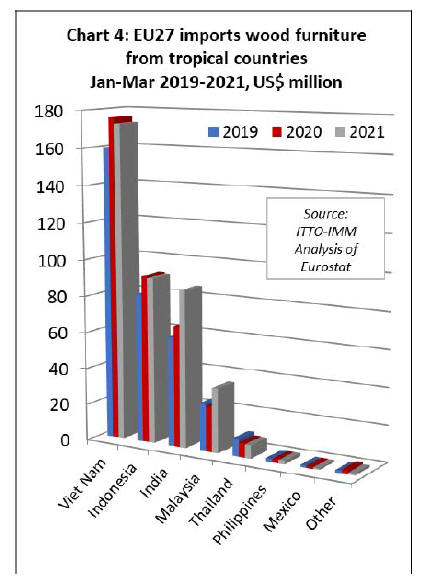

Rising EU27 wood furniture imports from India and

Malaysia

In the first three months of 2021 compared to the same

period in 2020, EU27 import value of wood furniture

increased sharply from India (+30% to US$86 million)

and Malaysia (+41% to US$35 million). However import

value from the two largest suppliers was marginally down

on the previous yearˇŻs level, declining 2% from Vietnam

to US$173 million and 1% from Indonesia to US$91

million (Chart 4).

It is notable that India, until recently only a relatively

minor supplier of wood furniture to the EU, is now

challenging Indonesia as the second largest tropical

supplier of these products into the region.

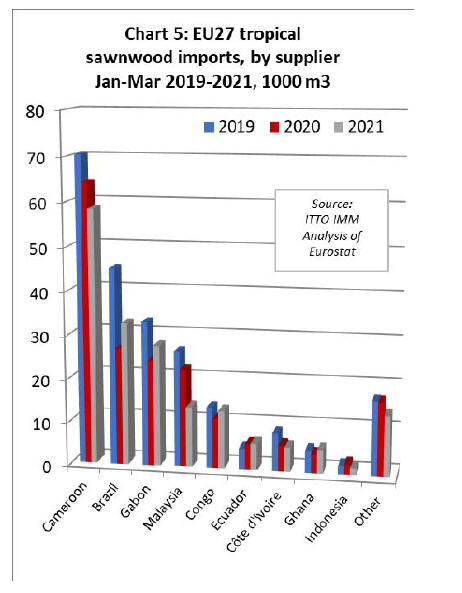

Sharp decline in sawnwood imports from Cameroon

and Malaysia

The EU27 imported 178,400 cu.m of tropical sawnwood

in the first three months of this year, 3% less than the same

period in 2020. Imports were sharply down from

Cameroon (-9% to 58,300 cu.m) and Malaysia (-38% to

13,900 cu.m), while imports from Côte dˇŻIvoire continued

a steady decline (-6% to 5,600 cu.m).

However, there were gains in imports from Brazil (+21%

to 32,500 cu.m), Gabon (+15% to 27,800 cu.m), Republic

of Congo (+17% to 13,300 cu.m), Ecuador (+5% to 6,100

cu.m), and Ghana (+27% to 5,400 cu.m). Despite the sharp

decline in imports from Cameroon this year and last, it is

notable that the country still remains very dominant as the

lead supplier of tropical sawnwood into the EU27 (Chart

5).

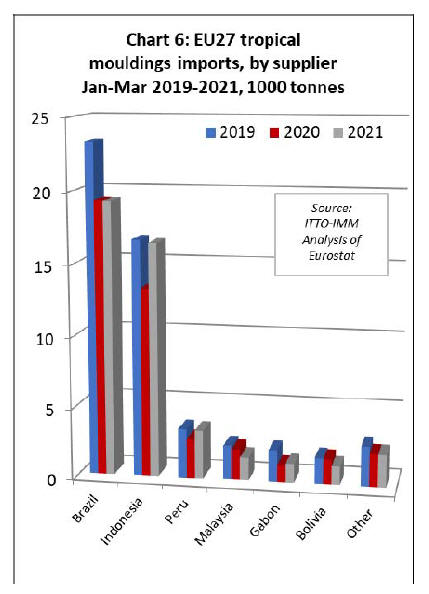

In contrast to sawnwood, EU27 imports of tropical

mouldings/decking increased in the first quarter of this

year, at 45,700 tonnes 7% more than the same period in

2020. Imports from Brazil, the largest supplier, were level

at 19,300 tonnes. Despite widespread reports of supply

shortages for Indonesian bangkirai decking, imports of

moulding/decking from Indonesia increased 24% to

16,400 tonnes during the three month period.

Imports also increased 24% to 3,400 tonnes from Peru and

11% to 1340 tonnes from Gabon. These gains offset a 26%

decline in imports from Malaysia to 1600 tonnes, and a

26% fall from Bolivia to 1,300 tonnes (Chart 6).

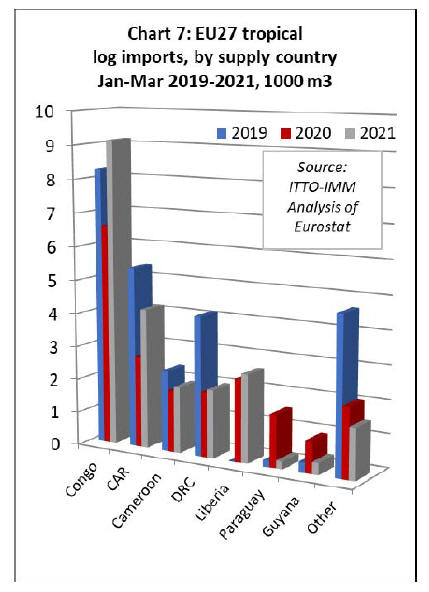

EU27 imports of tropical logs, which have been in long

term decline and are now a shadow of their former level,

did at least rebound 9% to 22,000 cu.m in the first three

months of this year. Imports recovered from the leading

African supply countries but imports from South

American countries, which had increased sharply last year,

fell back to negligible levels.

Imports increased 38% to 9,100 cu.m from the Republic of

Congo, 52% to 4,200 cu.m from CAR, 8% to 2000 cu.m

from Cameroon, 5% to 2,000 cu.m from DRC, and 7% to

2,600 cu.m from Liberia. In contrast, imports from

Paraguay fell 85% to just 236 cu.m and from Guyana were

down 27% to 360 cu.m (Chart 7).

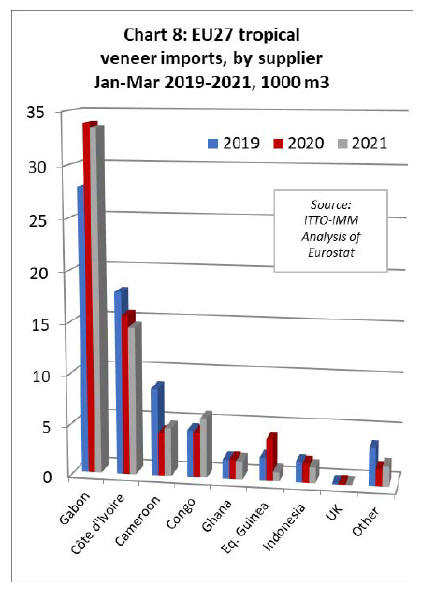

Slow start to the year for imports of tropical veneer

and plywood

EU27 imports of tropical veneer declined 4% to 64,900

cu.m in the first three months of this year. After a rapid

rise last year, imports from Gabon declined 1% to 33,500

cu.m. There were larger falls in imports from Côte d'Ivoire

(-7% to 14,500 cu.m), Ghana (-7% to 1,800 cu.m),

Equatorial Guinea (-78% to 900 cu.m), and Indonesia (-

17% to 1,537 cu.m).

However, imports increased 13% to 4,700 cu.m from

Cameroon and 32% to 5,900 cu.m from the Republic of

Congo (Chart 8).

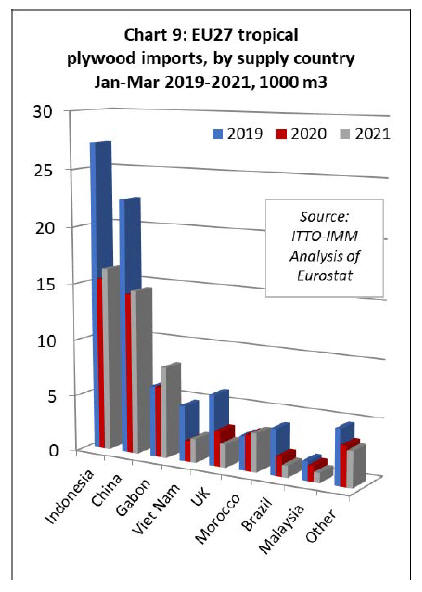

After a slow year in 2020, EU27 imports of tropical

plywood made only marginal gains in the first quarter of

this year. Imports of 51,500 cu.m in the three month

period were just 2% more than in the same period in 2019.

Imports were up from all four of the largest supply

countries including Indonesia (+6% to 16,200 cu.m),

China (+2% to 14,500 cu.m), Gabon (+29% to 8,000

cu.m), and Vietnam (+14% to 2,100 cu.m).

However, the decline in imports continued from Brazil (-

40% to 1,100 cu.m) and Malaysia (-37% to 875 cu.m.).

EU27 imports of tropical hardwood plywood from the UK

¨C a re-export since the UK has no plywood manufacturing

capacity ¨C fell 35% to 2,000 cu.m (Chart 9).

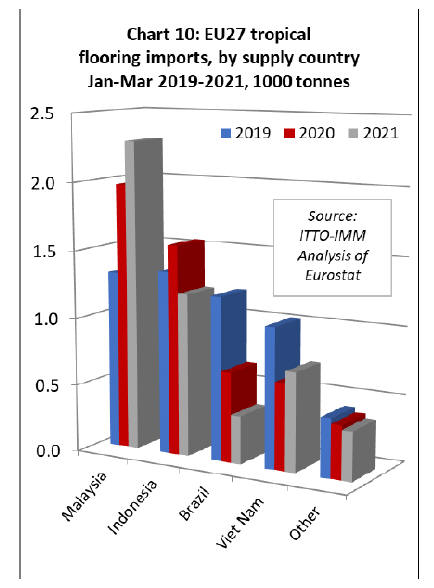

Tropical flooring imports rise while other joinery

imports decline

After unexpectedly recovering some lost ground last year,

EU27 imports of flooring from tropical countries have

weakened again this year. Imports of 4,900 tonnes in the

first three months were 6% less than the same period in

2020. Imports from Malaysia continued to rise, up 16% to

2,300 tonnes, while imports from Vietnam recovered by

13% to 730 tonnes.

However, these gains were offset by a 23% decline in

imports from Indonesia to 1,200 tonnes and a 47% decline

in imports from Brazil to just 360 tonnes. (Chart 10).

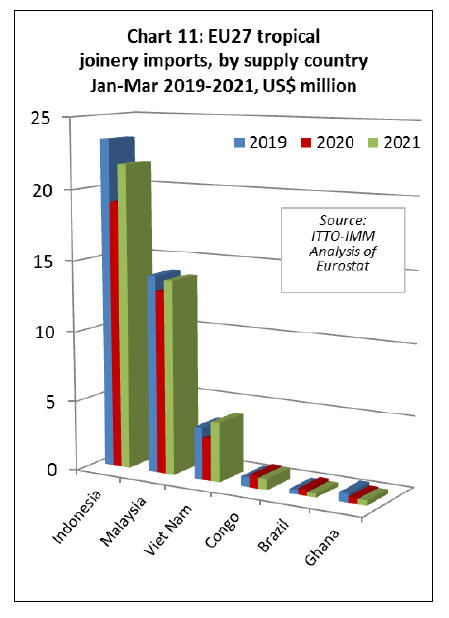

The value of EU27 imports of other joinery products from

tropical countries - which mainly comprise laminated

window scantlings, kitchen tops and wood doors -

increased 11% to US$43 million in the first three months

of this year.

Imports were up 22% to US$21.7 million from Indonesia,

6% to US$13.8 million from Malaysia, and 41% to

US$4.2 million from Vietnam (Chart 11).

Latest on EU policy framework for ˇ®forest-riskˇŻ

commodities

Speaking at a webinar hosted by the EURACTIV news

agency on 26 May, Virginijus Sinkevičius, EC

Commissioner for Environment, Oceans and Fisheries,

provided an update on the state of play in EU deliberations

on a new policy framework to ensure EU consumption is

not contributing to global deforestation and forest

degradation.

See:

https://events.euractiv.com/event/info/eu-agenda-for-globalforests-getting-the-balance-right

The Commissioner reiterated the EUˇŻs intention to

develop new laws to prevent commodities with a high risk

of contributing to deforestation being placed on the EU

market.

The EU is also likely to propose that these new laws be

implemented alongside new partnerships with countries

supplying ˇ°forest riskˇ± commodities to develop procedures

to ensure that products are ˇ°deforestation freeˇ±.

ˇˇ

The Commissioner began by emphasising that the whole

issue of deforestation is ˇ°high on the political agenda, it's

very high on the Commission's agenda, it's an important

matter for companies, NGOs and of course citizens, and

it's a key topic for everyone on the ground in the

producing countriesˇ± and noted that ˇ°tackling

deforestation is an important element in [the] European

Green Dealˇ± (which sets out the trajectory for the EU to be

climate neutral by 2050).

The Commissioner said that the intention was to build on,

and learn from, existing forest policy mechanisms,

particularly those implemented as part of the FLEGT

Action Plan.

He noted that ˇ°part of the process to develop a new

legislative proposal is an evaluation of the effectiveness of

existing legislation; a fitness check of both the EU Timber

Regulation and the FLEGT Regulation with its Voluntary

Partnership Agreementsˇ±. He also said the EC is

ˇ°conducting a study on the role and impact of private

certification schemes, and the contributions they could

make to additional measuresˇ±.

Commenting on the role of the EUTR, the Commissioner

said that ˇ°a mixed picture is emerging; it has been an

incentive for operators to focus on keeping their supply

chains clean, but the structure and the wording of the

legislation has made it difficult to use in practice. The

[EUTR] competent authorities found it hard to prove due

diligence compliance failures in courts of law. In that area

there is definitely room for improvementˇ±.

On the role of the VPAs, the Commissioner said that these

ˇ°have clearly proved their use in improving stakeholder

participation, better forest governance and regulatory

reforms in some partner countries, but their actual impact

on illegal logging and associated trade has been more

limited. We have not found much evidence that these

agreements have helped reduce illegal logging or the

consumption of illegally harvested wood here in Europeˇ±.

The Commissioner emphasised that this was not intended

as a criticism of progress made in any individual VPA but

rather the ˇ°problem is simply one of scale; the first VPA

was concluded with Ghana more than a decade ago, but

today when we have 15 different VPAs at various stages

of completion, there is only one operating licencing

system in place in Indonesia. That means that despite our

best efforts, these agreements cover only a very small part

of the overall volume of trade. So the total effect on illegal

timber is therefore extremely limitedˇ±.

The Commissioner went to say that ˇ°these conclusions

together with the feedback from extensive public

consultations, input from the European Parliament, and

studies we have carried out, are quite clear. The current

system of due diligence needs to be improved and

enhanced, but that alone will not be enoughˇ±.

According to the Commissioner, ˇ°enhancedˇ± due diligence

ˇ°will need to be complemented by alternative support

methods which help partner countries to comply with the

requirementsˇ±. He indicated that there would be a more

flexible approach to development of forest partnership

agreements so that they are ˇ°tailored to specific needs and

the specific interests of each partner countryˇ±.

This implied that the agreements ˇ°should retain the

elements that have proved effective, while other

[elements], like licencing in a trade agreement, should be

abandoned.ˇ± Perhaps hinting at a shift towards more

jurisdictional forms of verification based on analysis of

governance and assessment of forest condition at national

or regional level, he noted that ˇ°we are also creating an

EU Observatory which will facilitate information

exchange on global deforestation, combining trade data

with [satellite] observationˇ±.

In finalising their regulatory proposals, the Commissioner

said ˇ°we need to be certain that all options comply with

our obligations under the World Trade Organisation

rulesˇwe started with a long list of 20 options, now we

are down to a few ones such as improved due diligence

requirements, country benchmarking, mandatory public

certification, mandatory labelling, or a deforestation free

requirementˇ±.

He also said that the EC identified a ˇ°preliminary list of

products, the main criteria for choosing them [being] the

overall impact of production and harvesting on forests and

their level of consumption in the EU, so that list includes

for now palm oil, cattle, soy, wood, cocoa and coffeeˇ±.

The Commissioner concluded that ˇ°we have come a long

way since the first commission proposal in its 2019

communication [on Stepping up EU Action to Protect and

Restore the World's Forests]. Under the Green Deal we are

advancing steadily and we are advancing with care. We

have no choice but of course to get it right. And for that to

happen, we need to listen to the views from all sidesˇ±.

|