US Dollar Exchange Rates of

10th

March

2026

China Yuan 6.88

Report from China

2025 real estate and retail sales developments

The National Bureau of Statistics (NBS) of China has

issued two press releases, one on the 2025 real estate

sector and the other on Retail Sales of Consumer Goods in

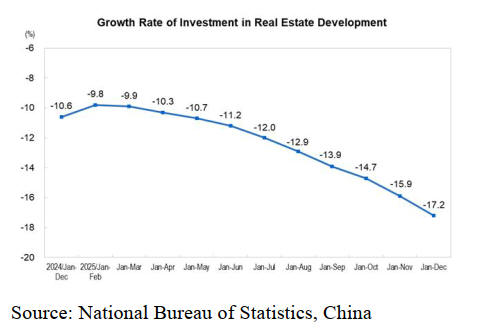

December 2025. The NBS says in 2025 investment in real

estate development decrease of 17.2%, of which

investment in residential buildings was down 16.3%.

In 2025 retail sales of convenience stores, supermarkets,

department stores and specialty stores among retail

enterprises increased by 5.5%, 4.3%, 0.1%, 2.6%

respectively year on year, those of brand-exclusive stores

declined by 0.6% year on year.

Online retail sales in 2025 were up by 8.6% year on year.

Specifically, online retail sales of physical goods were

higher by 5.2% and accounted for 26% of the total retail

sales of consumer goods.

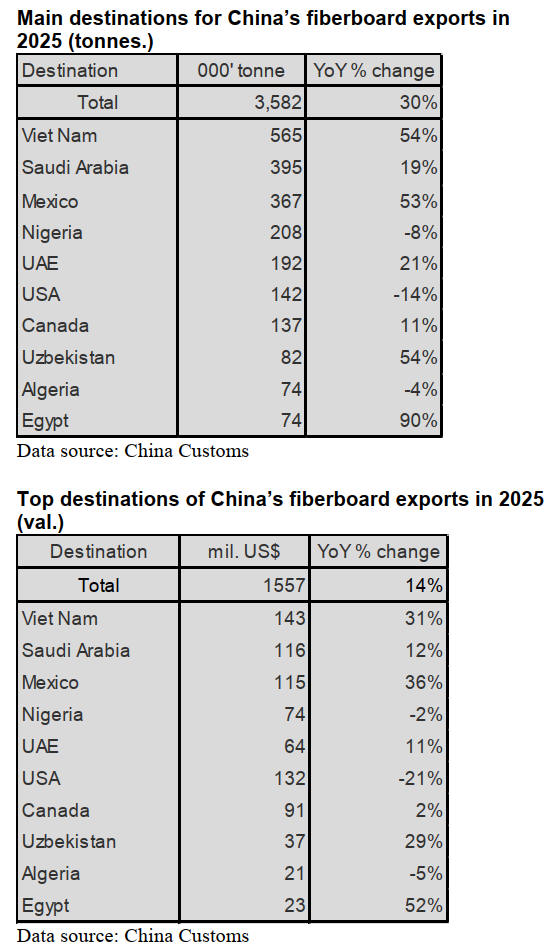

Growth in fibreboard exports

According to China Customs, China’s fibreboard exports

in 2025 grew 30% to 3.582 million tonnes valued at

US$1.557 billion, up 14% year on year.

China’s fibreboard exports to Viet Nam as the largest

destination in 2025 rose over 50% to 565,000 tonnes year

on year. Fibreboard exports to Saudi Arabia as second

largest destination in 2025 rose 19% to 395,000 tonnes

year on year.

In addition, China’s fibreboard exports to Mexico, UAE,

Canada, Uzbekistan and Egypt rose 53%, 21%, 11%, 54%

and 90% respectively compared to 2024 levels. In

contrast, China’s fibreboard exports to Nigeria, USA and

Algeria dropped 8%, 14% and 4% respectively on 2024.

The production capacity of fiberboard in China has been

continuously decreasing in recent years. Producers rely on

diversified international markets with domestic demand

accounting for only a fraction of the trade. China’s

fibreboard exports have experienced a significant increase

in 2025.

At the end of 2025 there were 220 fibreboard mills across

the country with a total of 244 production lines. The total

annual production capacity was 40.4 million cubic metres.

Compared with the situation at the end of 2024 capacity

decreased by 3%, representing a continuous decline for

four consecutive years.

Domestic demand has limited impact on China’s

fibreboard trade. Although the domestic home furnishing

industry is forecast at RMB15 trillion in 2025 the demand

for fibreboard is driven by urbanisation and environmental

protection policies. However, the real estate market has

not shown a significant recovery and the transmission

effect of domestic demand on fibreboard exports is

relatively weak.

The growth of China's fiberboard exports mainly relies on

diversification in emerging markets rather than a single

market boom. By 2025, China's fiberboard exports have

faced structural pressures such as trade friction, capacity

contraction and rising costs. Despite these challenges,

China’s fibreboard exports maintained a relatively stable

growth in 2025.

Rise in fibreboard imports

According to China Customs, China’s fiberboard imports

rose 12% to 60, 000 tonnes valued at US$44 million in

2025, down 6% year on year. New Zealand was the largest

suppliers in 2025. China’s fibreboard imports from New

Zealand rose 68% to 28,000 tonnes on 2024 levels and

accounted for 47% of national imports.

The main reasons for the significant increase in China's

imports of New Zealand fiberboard is that the quality of

New Zealand radiata pine fibreboard is stable and the

maritime transportation route is mature with a high level

of supply chain reliability.

The upgraded China-New Zealand Free Trade Agreement

will gradually eliminate tariffs on 12 categories of wood

and paper products (including wood fibreboard) over a

period of 10 years significantly enhancing the price

competitiveness of New Zealand's fibreboards in the

Chinese market.

75% of China’s fibreboard was imported from 4 countries

in 2025, namely New Zealand, Thailand, Germany and

Romania.

China’s fibreboard imports from Romania in 2025 grew

8% to 5,100 tonnes year on year. In contrast, China’s

fibreboard imports from Thailand and Germany in 2025

dropped 35% and 22% respectively on 2024 level. It is

worth noting that China’s fiberboard imports from

Australia and Malaysia in 2025 surged over 160% and

nearly 500% respectively year on year.

In contrast, China’s fiberboard imports from Belgium and

Switzerland in 2025 fell 27% and 28% respectively on

2024 level.

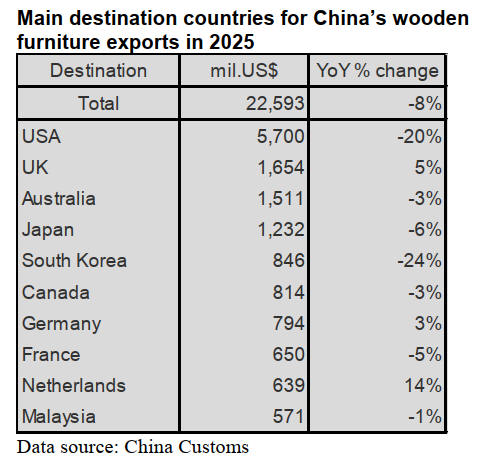

Decline in wooden furniture exports

China Customs data shows the value of China's wooden

furniture exports in 2025 dropped 8% to US$22.593

billion year on year. The USA was is the largest market

for China’s wooden furniture exports with around 25% of

China’s wooden furniture being shipped to the US valued

at US$5.7 bil. in 2025, down 20% on 2024.

The decline in China's furniture exports in 2025 was

mainly attributed to the trade friction between China and

the United States.

China’s wooden furniture was exported to more than 200

countries in 2025. The value of China’s furniture exports

to the top 4 countries the USA, UK, Australia and Japan

with furniture exports of more than US$1 billion,

accounted for 45% of the national total in 2025.

The value of China’s wooden furniture exports to UK and

Netherlands in 2025 rose 5% and 14% respectively year

on year. In contrast, the value of China’s wooden furniture

exports to the rest of the top destination countries in 2025

dropped at different rates on 2024 level.

Decline in wooden furniture imports

The value of China’s wooden furniture imports in 2025

fell 7% to US$609 million year on year. Italy, Germany

and Viet Nam were the top three suppliers. 67% of

China’s wooden furniture were imported from those 3

countries but imports fell 7%, 19% and 23% respectively

in 2025. This is the main reason for the decrease in the

overall value of China’s wooden furniture imports in 2025.

The main reason for the large decline in China's furniture

imports is that domestic demand for furniture has fallen

sharply due to the downturn in China's real estate market.

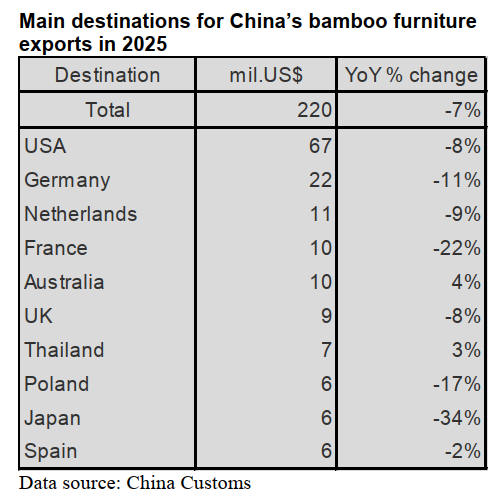

Decline in Bamboo furniture exports

The value of China’s bamboo exports in 2025 dropped 7%

to US$220 million year on year. The value of bamboo

furniture exports to the USA, as the largest destination, fell

8% year on year and accounted for 31% of the national

total furniture export value in 2025.

Also, the value of China’s bamboo furniture exports to

Germany, France, Poland and Japan dropped 11%, 22%,

17% and 34% respectively year on year. In contrast,

China’s bamboo furniture exports to Australia and

Thailand rose 4% and 3% year on year.

The main reasons for the decrease in the value of Chinese

bamboo furniture exports were as follows:

The United States has continuously imposed tariffs

on Chinese wood products, especially placing

significant pressure on traditional categories such as

wooden and bamboo furniture.

Many countries have initiated anti-dumping

investigations and implemented technical trade

barriers (such as environmental standards and wood

legality certifications) against Chinese furniture,

increasing the compliance costs for enterprise

exports.

Major consumer markets such as Europe and the

United States are affected by high inflation and high

interest rates, resulting in weakened consumer

willingness to buy home furnishings, thereby putting

pressure on the export of non-essential products like

bamboo furniture.

Although the dependence on the United States has

been decreasing year by year, the United States

remains the largest buyer and the high market

concentration brings risks.

Some bamboo furniture enterprises still mainly

engage in OEM (Original Equipment Manufacturing)

with low proportions of their own brands and high

value-added products, making it difficult for them to

respond to changes in high-end market demands.

Decline in bamboo furniture imports

According to China Customs, the value of China’s

bamboo furniture imports in 2025 fell 26% to US$1.739

billion year on year.

Indonesia was the largest supplier of China’s bamboo

furniture imports in 2025 but imports from Indonesia in

2025 fell 18% on 2024 levels and this directly resulted in

the overall decline in imports.

87% of China’s bamboo furniture were imported from

Indonesia, Viet Nam and Italy in 2025 but declined 18%,

14% and 5% respectively year on year.

|