Japan

Wood Products Prices

Dollar Exchange Rates of 25th

March

2026

Japan Yen 160.03

Reports From Japan

Widespread energy disruptions

Japan is experiencing widespread energy disruptions as the

conflict in the Middle East limits oil flows through key

supply routes such as the Strait of Hormuz. With around

90% of its oil imported from the region, industries

including steel, petrochemicals and refining are reducing

operations due to shortages and rising costs.

The government has released emergency stockpiles and

introduced subsidies to stabilise fuel prices. However,

businesses ranging from heavy industry to small public

bathhouses are being impacted. The crisis is also

prompting discussions around diversifying energy imports,

increasing coal usage and reconsidering nuclear power as

a long-term energy solution.

Japan began to release oil from its reserves to alleviate

supply concerns that have grown amid the conflict with

Iran and stabilise the distribution of petroleum products.

The release by Japan for its domestic market came ahead

of a planned coordinated release by the 32 countries of the

International Energy Agency, including Japan. At the end

of 2025 Japan held reserves of approximately 470 million

barrels of oil, equivalent to 254 days of domestic

consumption, of which 146 days' worth were government-

owned, 101 days held by the private sector, and the

remainder jointly stored by oil-producing countries.

Japan imports more than 90 percent of its crude oil from

the Middle East, making it highly vulnerable to the

effective closure of the Strait of Hormuz, which has

prevented the transportation of oil and gas from causing

sharp rises in crude oil prices.

See: https://impakter.com/japan-energy-crisis-middle-east-

supply-disruption/

and

https://asia.nikkei.com/business/energy/japan-begins-oil-reserve-

release-amid-iran-crisis

In related news, after three decades of deflation, Japan has

pivoted to sustained inflation with consumer prices rising

nearly 3%, exceeding the Bank of Japan's 2% target for

over 30 consecutive months as of early 2026.

Driven by a weak yen, rising wages and high import costs,

this historic shift marks a potential end to the "lost

decades," forcing a normalisation of monetary policy away

from negative interest rates. The depreciation of the yen

has drastically increased the cost of imported fuel, raw

materials and food, passing higher costs to consumers.

Interest rate increase delayed

Rising oil prices, weak wage data and the weak yen have

complicated Japan's monetary policy direction. High oil

prices will likely negatively impact the economy and spur

inflation and this comes at a time when the Bank of Japan

has to started to normalise polcy direction.

The Bank of Jpan (BoJ) governor Kazuo Ueda said at a

press conference after its two-day policy meeting that he

"needs more time" to understand the impact the war will

have on the economy.

"We have decided to keep the policy unchanged as risks

associated with rising crude oil prices have newly

emerged," he said, adding "We will make an appropriate

policy decision in April after examining the risk scenario

and outlook as more data become available."

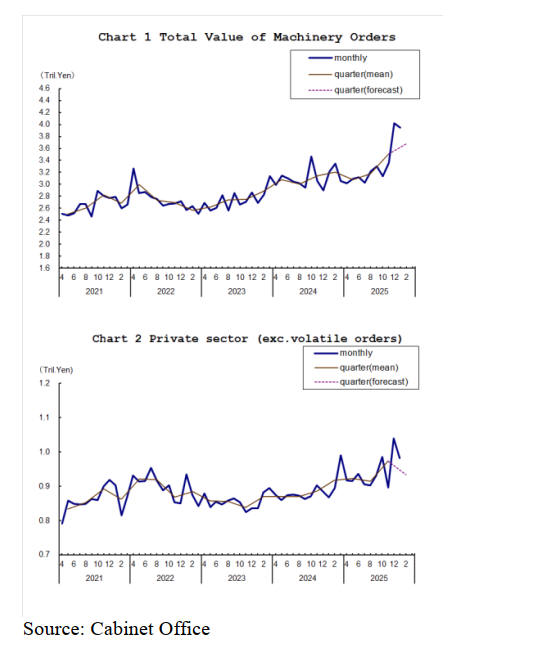

Capital spending to remain firm but concerns remain

Japan's seasonally adjusted core machinery orders in

January fell 5.5% from the previous month, after a spike

driven by large-scale orders in December, according to

Cabinet Office data.

The private-sector orders, excluding those for ships and

equipment used at power companies, closely watched as a

leading indicator of corporate capital spending declined.

The Cabinet Office maintained its assessment, saying that

machinery orders are showing signs of picking up. Many

private think tanks expect corporate capital spending to

remain firm, but concerns remain over the conflict in Iran.

See: https://www.esri.cao.go.jp/en/stat/juchu/juchu-e.html

and

https://www.japantimes.co.jp/business/2026/03/19/economy/japa

n-machinery-orders-january/

Labour unions secure wage increases

Domestic consumption is projected to be a primary driver

of Japan's economic growth in 2026 with real GDP

expected to grow by approximately 1.3% to 1.48%. This

growth is anticipated to be fueled by a cycle of wage

increases exceeding inflation, improving household

disposable income and government measures designed to

support consumption.

As of 23 March 2026, Japanese labour unions secured an

average annual wage increase of 5.26% in the preliminary

spring "Shunto" negotiations, a development that likely

will keep theBank of Japan on track for another interest

rate hike in the coming months.

This marks the third consecutive year of increases

exceeding 5% demanded to combat inflation and accepted

by the big companies as they face labour shortages. The

average 5.26% is slightly below 2025's 5.46%. Small and

mid-sized firms offered the unions 5.05%, missing the

union goal of 6% but still showing steady growth. These

figures will be revised several times as more companies

report results.

Sustained wage gains are needed to underpin consumption

and drive the demand-led price gains that the Bank of

Japan has been seeking as it pursues the conditions that

would allow it to normalise monetary policy.

Nobuyasu Atago, Chief Economist at Rakuten Securities

Economic Research Institute said “the results confirmed

the Bank of Japan’s baseline scenario that this year’s wage

negotiations have been solid”, adding “the key question is

how far the gains will spread to small and midsize firms”.

See:

https://www.japantimes.co.jp/business/2026/03/23/companies/re

ngo-labor-unions-wage-hikes/

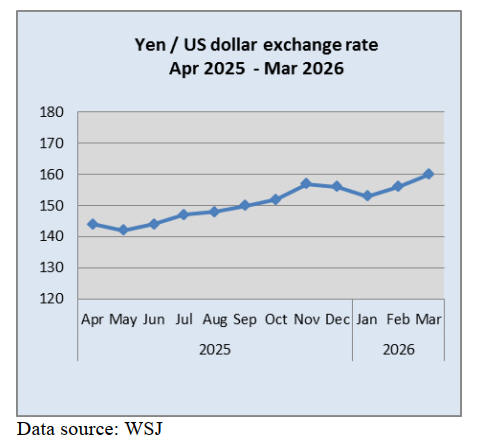

Posibility ofcurrency intervention rises

As the yen reached 160 to the US dollar level market

watchers are back on intervention watch. The US media

have said uncertainty has sparked safe-haven demand for

the US dollar. Now that 160 has been reached it is highly

likely the Japanese government will start yen buying.

Shortage of carpenters delaying home construction

A severe shortage of carpenters in Japan has reached

critical levels causing significant delays in residential

construction, driving up home prices and disrupting the

housing market. It has been estimated that he number of

carpenters has dropped to one-third of the 1980 peak with

projections indicating further declines.

Homebuyers are facing delays of more than six months

before construction can begin due to the shortage of

experienced workers. Data indicates over 40% of current

carpenters are over 65 years old and less than 20% are

younger workers. The sub-contacting system for

carpenters leads to long hours and unattractive pay deters

younger people from entering the profession. New

regulations on overtime work, introduced to reduce long

hours have worsened labour availability.

See: https://www.asahi.com/ajw/articles/15709629

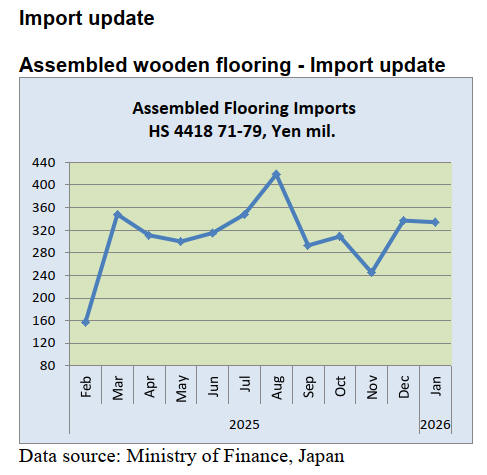

In December 2025 there was a reversal of the downward

trend seen in the previous three months and in January the

higher value of assembled wooden flooring (HS441871-

79) was maintained.

Year on year the value of January 2026 imports

declined

26% but compared to a month earlier the value of January

imports little unchanged.

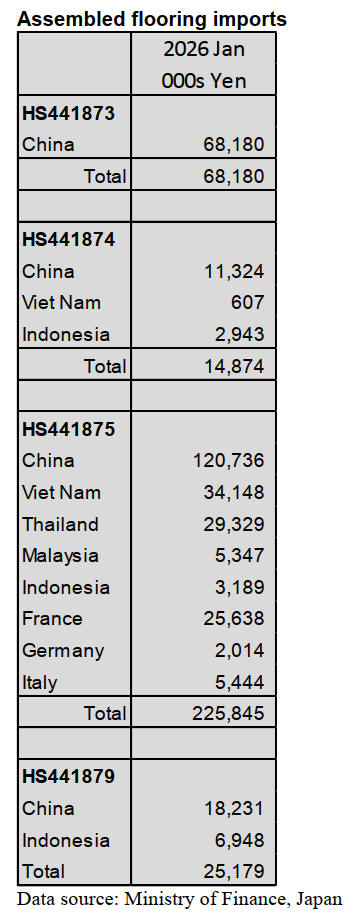

Of the various categories of assembled flooring imports in

January, 90% was of HS 441875, a significant jump

compared to the previous three months. Of HS441875

imports four countries accounted for over 90% of arrivals

with 53% from China, 15% from Viet Nam, 13% from

Thailand and 12% from France. However shipments from

France were down sharply comped to December.

All imports of HS4418-73 originated in China and

accounted for 20% of January arrivals, up from the

previous month. For the other categories HS441879

accounted for 7% in January (10% in December) followed

by HS441874 at 4%.

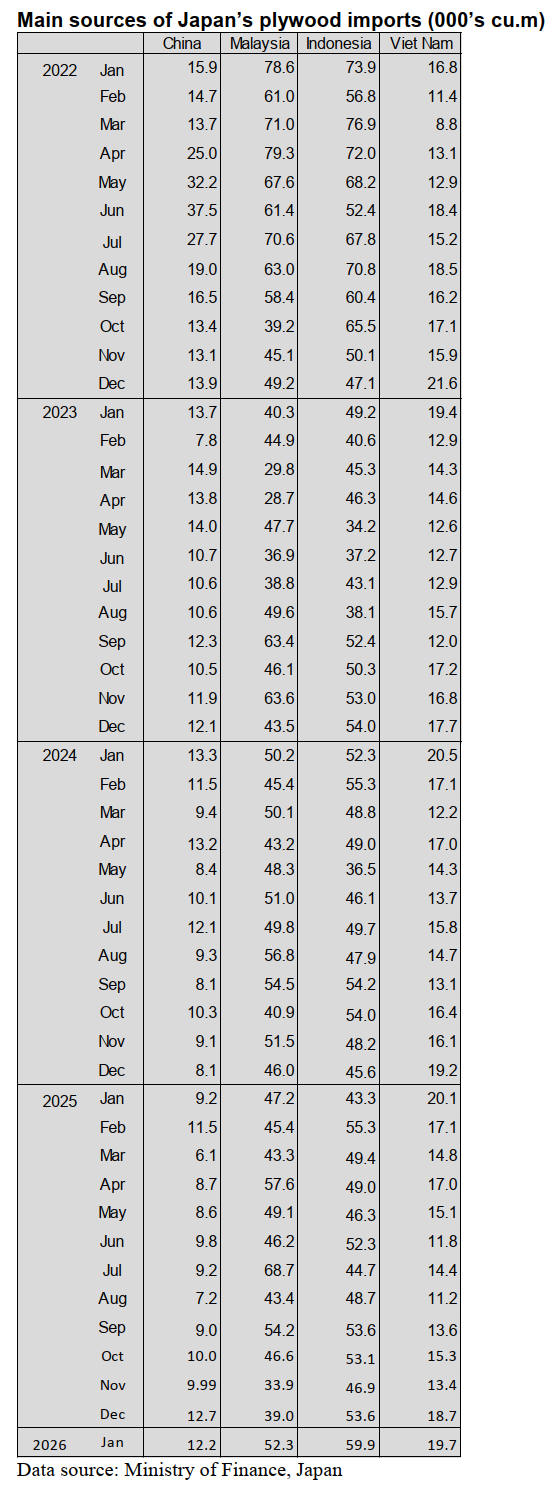

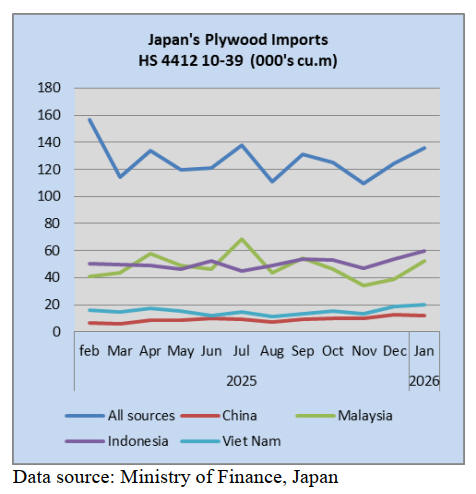

Plywood imports

In January 2026 Indonesia and Malaysia continued as the

top suppliers of plywood to Japan with the combined

volume of shipments from the two main shippers

accounting for 83% of January imports (74% in

December).

January shipments from Malaysia were up sharply

compared to the volume shipped to Japan in December

2025 where as shipments from Indonesia were at around

the same level as in December. The other top shippers of

plywood to Japan in January were Viet Nam and China.

January arrivals from Vietnam were up from the previous

month whereas arrivals from China were at around the

same level as in December.

Arrivals from China in December 2025 and 2026, at

around 12,000 cu.m per month, were noticeably higher

than the monthly average in 2025.

In January 2026 arrivals of HS441210-39 were reported at

135,803 cu.m (124,460 cu.m in December). As in previous

months, of the various categories of plywood imported in

January 2026, HS441231 accounted for most (81%)

followed by HS441233 and HS441234 at a consistent 6%

each with the balance being HS441239 and HS441210.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

Orders for house builders

The major homebuilders saw their order values in January

exceed those of the same month last year. However, this

was largely due to the weakness in orders a year earlier,

and it does not necessarily indicate an improvement in

demand conditions at the start of the year. With no rush of

last-minute demand expected this year—unlike in 2025,

when regulatory changes prompted early orders—

homebuilders are widely expected to face a challenging

environment in February and March.

The rental apartment segment performed well overall.

Amid expectations of rising interest rates, some consumers

are holding off on purchasing single-family homes and

instead shifting toward investment in rental properties.

The trend towards adding value and increasing the scale of

rental units has continued into the new year.

Wood products from NZ and Chile in 2025

In 2025, imports into Japan of New Zealand radiata pine

logs and Chilean radiata pine lumber both posted double-

digit declines, falling even further below the record-low

levels seen in 2024. The decline in imports has continued

for three consecutive years.

Although the yen’s depreciation eased last year, rising

ocean freight rates, port-handling charges, and warehouse

fees kept selling prices elevated, leading to a continued

shift in demand toward more affordable and readily

available Japanese cedar products. In the first half of the

year, international logistics delays and trade stagnation—

driven in part by the Trump tariffs—further dampened

industrial demand for wood-based packaging materials, as

demand for export crates and other industrial applications

weakened.

Imports of New Zealand radiata pine totaled 208,146

cbms, down 12.8% from the previous year, falling to less

than one-third of the recent peak of 723,000 cbms

recorded in 2012. Imports of Chilean radiata pine came to

142,125 cbms, a steep 16.5% drop from the previous year,

falling to less than half of the recent peak of 330,000 cbms

recorded in 2018.

Because about 90% of New Zealand radiata pine is

exported to China, prices for the Japanese market tend to

track Chinese market conditions. In mid-2025, prices for

China-bound shipments briefly fell to as low as US$105

per cbm on a C&F basis, one of the lowest levels seen in

the market. However, the weak yen kept import costs from

declining, accelerating the shift in demand toward more

affordable Japanese cedar.

Although Chilean lumber continued to arrive under the

same five-vessel framework as the previous year, major

producer CMPC shifted from joint bulk-vessel shipments

with Arauco to its own container-based transport. As a

result, Arauco was left to operate vessels on its own,

leading to an increase in mixed cargoes with pulp and

other products and pushing up ocean freight costs.

Consequently, upward pressure on the cost of Chilean

lumber has intensified.

Imported wood fuel in 2025

Japan’s imports of woody biomass fuels reached 15.739

million tonnes in 2025, including wood pellets and PKS,

marking a 26.9% increase from the previous year and

underscoring continued robust growth in demand.

Imports of wood pellets rose by just over 30% from the

previous year, while arrivals of PKS increased by slightly

under 20%. However, the gap between the two fuels

widened sharply, from 355,000 tonnes in 2024 to 1.535

million tonnes in 2025, as wood pellets saw a substantial

surge in demand, driven in part by their higher combustion

efficiency and other performance advantages.

The sharp increase in imports was driven in part by the

launch of several large-scale biomass power plants with

capacities exceeding 50,000 kW across Japan in 2025,

which significantly boosted demand for imported woody

fuels.

Imports of wood pellets totaled 8.637 million tonnes in

2025, representing a 35.4% increase from the previous

year. By country of origin, Vietnam remained the

dominant supplier with 5.682 million tonnes, up 71.4%

from the previous year.

It was followed by Canada with 1.292 million tonnes, a

10.8% increase, the United States with 676,000 tonnes, up

39.5%, Malaysia with 472,000 tonnes, up 17.1%, and

Indonesia with 404,000 tonnes, up 28.5%.

Imports of PKS came to 7.102 million tonnes, an increase

of 17.9% from the previous year.

By country of origin, imports totaled 5.515 million tonnes

from Indonesia, up 19.9% from the previous year; 1.479

million tonnes from Malaysia, a 7.1% increase; and

107,000 tonnes from Thailand, which surged 136.7% year

on year.

Although the latest FIT-certified installation data compiled

by the Agency for Natural Resources and Energy only

runs through June 2025, the number of operating facilities

in the general wood category had reached 113, up 12 from

the same month a year earlier. Total operating capacity

also increased to 9.91114 million kW, a year-on-year rise

of 662,690 kW.

Plywood

Shipments of domestically produced softwood structural

plywood remain sluggish across both traditional

distribution channels and precut factories, weighed down

by weak housing starts and buyer reluctance following

months of declining prices.

In February, several domestic manufacturers announced

price hikes for 12 mm, 3×6 plywood from March

shipments due to rising log and labor costs. This prompted

some buyers to advance purchases, though many remain

cautious, leaving market sentiment mixed.

Tokyo prices stand at ¥1,040–¥1,050 per sheet, with a firm

tone. Imported tropical plywood faces upward pressure

from Indonesian suppliers, especially for standard grades,

as natural-timber levies rise. Modest price increases have

been accepted after negotiations with Japan.

Malaysian producers, however, cannot raise prices due to

weak Japanese demand and currency-related cost

pressures. Indonesian export prices remain around

US$970/m³ for 2.4 mm, US$880/m³ for 3.7 mm, and

US$850/m³ for 5.2 mm. Indonesian export prices remain

around US$970/m³ for 2.4 mm, US$880/m³ for 3.7 mm,

and US$850/m³ for 5.2 mm, with 12 mm products

unchanged.

Domestic demand for imported plywood is subdued,

particularly for coated formwork plywood. Importers need

higher selling prices to cover costs but increases remain

limited. Current domestic prices range from ¥1,840–

¥1,900 for coated formwork plywood 12 mm to around

¥1,600 for formwork and structural plywood, and ¥780–

¥1,100 for Indonesian standard plywood depending on

thickness.

Domestic lumber and logs

Domestic cedar products are showing stronger price

momentum in the Kanto market as supply to precut plants

tightens. Although demand from major homebuilders has

eased since peaking in November–December 2025, orders

remain active, while local distribution channels continue

to stagnate.

With supply tightening since late last year, wholesalers

have raised prices, and standard KD cedar posts now trade

at ¥55,000–57,000 per cbm—about ¥2,000 higher than last

month—as mills in northern Kanto struggle to keep up.

Competing engineered wood products have also risen,

with laminated whitewood posts at ¥78,000–80,000 and

cedar laminated posts around ¥66,000, creating room for

further increases in solid cedar posts. Demand for cedar

studs is similarly strong, and limited supply of 45 mm

material has pushed prices above ¥65,000.

In contrast, the cypress log market remains weak outside

Okayama, where shortages have lifted prices. Cypress sill-

grade logs trade at about ¥23,000 per cbm in Okayama,

compared with ¥21,000 in Kyushu, ¥20,000 in Shikoku,

and ¥19,500 in northern Kanto—¥3,000–4,000 below last

autumn and ¥5,000–6,000 lower than a year earlier. The

decline reflects reduced demand amid sluggish product

markets rather than increased supply, as cedar log prices

remain firm.

While prices may rebound if demand recovers, a return to

last year’s unusually high levels appears unlikely. Cedar

medium-diameter logs remain stable at ¥16,000 in Akita

and northern Kanto and ¥14,000–14,500 in Kyushu.

Compared with a year earlier, prices are slightly lower in

Kanto and Kyushu but ¥2,000 higher in Akita, raising

attention as to whether a new price level is emerging.

Japan to revise formula for calculating wood self-

sufficiency rate

Japan’s Forestry Agency has proposed revising the

formula used to calculate the nation’s wood self-

sufficiency rate, aiming to provide a more accurate picture

of domestic supply. The proposal was presented at a

meeting of the Forestry Policy Council held at the

agency’s headquarters on February 20.

Under the current method, wood exports are included in

the denominator of the calculation, which can make the

self-sufficiency rate appear lower than the actual level of

domestic consumption. The agency now plans to exclude

export volumes from the denominator, effectively aligning

the metric with wood used within Japan. The revision is

intended to better reflect domestic supply-and-demand

conditions as the country seeks to expand the use of

domestically sourced timber.

The agency says the revision is necessary because Japan’s

heavy reliance on imported timber has exposed

vulnerabilities in the country’s wood supply. As these

risks become more apparent, accurately measuring the

contribution of domestically produced timber to national

consumption has grown increasingly important.

Under the current formula, exports are included in the

denominator on the grounds that it reflects the contribution

of domestically produced timber to Japan’s wood-related

industries. The agency also plans to revise the log-

conversion coefficients used to estimate the volume of

imported timber and other wood products.

|