|

Report from

Europe

Another all-time low for UK tropical wood product imports

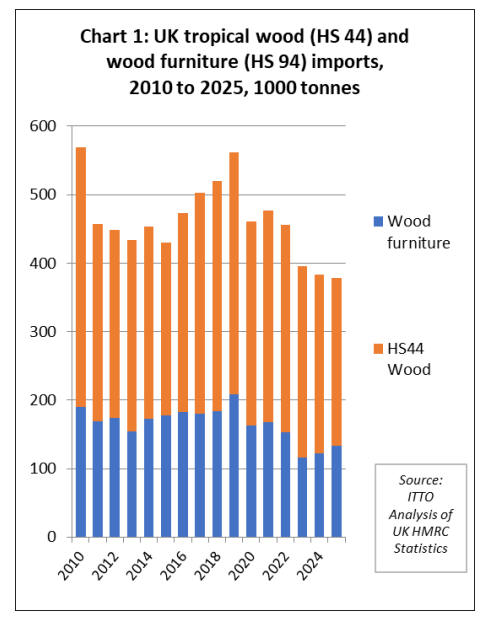

In 2025, the UK imported 377,900 tonnes of tropical wood

and wooden furniture products, 1.4% less than the

previous year. Although import value last year, at

US$1007.3 million, was 1.4% more than the previous year

in nominal terms, it was down 1% in real terms (taking

account of inflation).

In tonnage terms this was the lowest on record and, in

retrospect, may be seen as a continuation of a long-term

downward trend that started as far back as the 2008

financial crisis (Chart 1).

Import quantity last year was around half the level of

tropical wood imports into the UK typical two decades

ago. There was an upturn in UK tropical wood product

imports in 2015-2019, and another rebound in 2020-2022,

but these trends were driven respectively by a big increase

in imports of plywood faced with tropical hardwoods from

China, and then by the short-lived post-COVID boom.

While last year saw an increase in the quantity of UK

imports of wooden furniture from tropical countries(+9%

to 133,600 tonnes), mouldings/decking (+3% to 9,700

tonnes), flooring (+46% to 3,100 tonnes), and kitchenware

(+9% to 2,500 tonnes), there was a decline in imports of

tropical plywood (-8% to 87,100 tonnes), joinery products

(-3% to 72,100 tonnes), sawnwood (-6% to 55,500

tonnes), sleepers (-12% to 2,700 tonnes), and picture

frames (-19% to 2,300 tonnes).

UK imports of tropical wood and wooden furniture in the

fourth quarter of 2025 were 93,339 tonnes, 5% more than

the previous quarter, when imports of only 88,500 tonnes

were close to an historical low. UK tropical imports in Q4

2025 were down 8% compared to the same quarter the

previous year.

Tropical wood products underperformed in UK

The UK market for tropical wood and wooden furniture

last year was significantly slower than the wider UK

market for these products. UK import value of wood and

wooden furniture from all supply regions was US$11.35

billion in 2025, 4% more in real terms compared to the

previous year. The share of tropical wood and wooden

furniture products in total UK import value declined from

9.5% in 2024 to just 9.0% during 2025. This share is now

well down on the 11.4% share achieved in 2022 and close

to 14% share typical before the COVID pandemic.

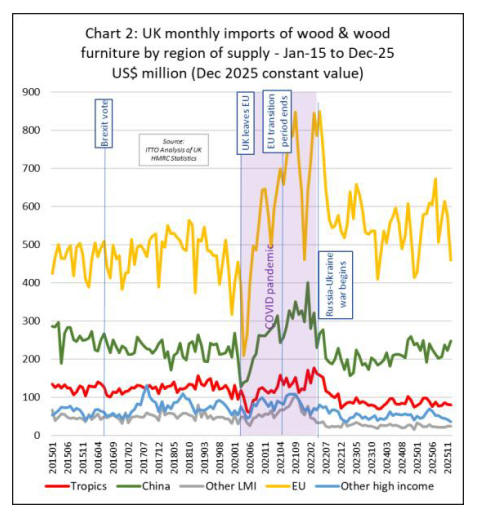

Considering the value of UK imports of all wood and

wooden furniture products in 2025, imports from China

were, at US$2.70 billion, 5% more than in 2024. China’s

share of total UK import value was 23.8% in 2025,

marginally up from 23.7% in 2024. Wood and wooden

furniture imports from the EU increased their dominance

of the UK market last year, rising 6% to US$6.71 billion.

Imports from the EU accounted for 59.1% of all UK

import value of wood and wooden furniture in 2025, up

from 58.4% share in 2024.

The most notable recent trend in the UK market for wood

and wooden furniture was a step change during the

COVID pandemic as the country became generally more

reliant on regional suppliers in Europe.

This trend ran contrary to expectations following the UK’s

departure from the EU in 2020 which led to speculation

that the country might turn more to alternative suppliers

outside Europe. UK imports from China recovered ground

in 2024 following a downturn in the immediate aftermath

of the pandemic, but this trend lost impetus in 2025 (Chart

2).

UK growth forecasts slashed on fears of interest rate increases

Prospects for any improvement in the UK market now

seem very slim. According to the Times of London, City

analysts are significantly reducing GDP estimates and

raising their forecasts for inflation. There is also little

room for the government to offer significant financial

support for households that will see their costs rise

because of the war in the Middle East.

Oxford Economics said that it now expected the UK

economy to expand by just 0.4 per cent this year, down

from its prior projection of 0.9 per cent. The research

consultancy also said that GDP would rise by 1 per cent

next year, down from its previous prediction of 1.3 per

cent.

“We expect a larger rise in inflation over the next year to

result in a more pronounced slowdown in activity growth,”

analysts wrote in a note to clients, adding that inflation

would peak at 4.1 per cent in the summer, more than

double the Bank of England’s 2 per cent target.

Deutsche Bank now believes that UK interest rates will

stay at 3.75 per cent for the rest of the year, having

previously predicted a handful of reductions.

However, the Times suggests other analysts are even more

pessimistic: “Markets now suggest that the Bank could lift

borrowing costs three times this year to 4.5 per cent from

3.75 per cent now, having just last month expected three

interest rate cuts”. This at a time when UK borrowing

costs are already at an 18 year high.

The latest data from the UK construction sector is

particularly troubling for UK wood demand. According to

the latest data from the UK Office of National Statistics,

total construction output in the UK is estimated to have

fallen by 2.0% in the three months to January 2026; this is

the fourth consecutive fall in the three-monthly series.

Over the three-month period, both new work, and repair

and maintenance, fell by 3.2% and 0.4%, respectively.

At the sector level, seven out of the nine sectors fell in the

three months to January 2026; the main negative

contributor to the decrease was private new housing,

which fell by 6.3%.

Monthly construction output is estimated to have grown

by 0.2% in January 2026; this follows three consecutive

falls in the monthly series. The increase in monthly output

in January 2026 came solely from an increase in repair and

maintenance, which grew by 3.3% as new work fell by

2.0%.

Sharp rise in wooden furniture from Vietnam

While the UK furniture market was far from buoyant, the

efforts of some tropical suppliers to diversify markets in

the UK in response to US tariff pressure are beginning to

pay off. In 2025, UK import value of wooden furniture

from tropical countries increased 11% in nominal terms to

US$506 million while import quantity increased 9% to

133,600 tonnes.

Wooden furniture imports from tropical countries

increased particularly sharply from Vietnam (+20% to

US$282.6 million), building on momentum that built up in

the second half of 2024.

Imports increased at a more moderate pace from Malaysia

(+3% to US$111.7 million), and Indonesia (+3% to

US$43.3 million). Imports from India were unchanged at

US$53.4 million.

However, imports declined from Thailand (-21% to

US$7.1 million), and Singapore (-20% to US$4.3 million).

UK wooden furniture imports were negligible from all

other tropical countries in 2025 (Chart 3).

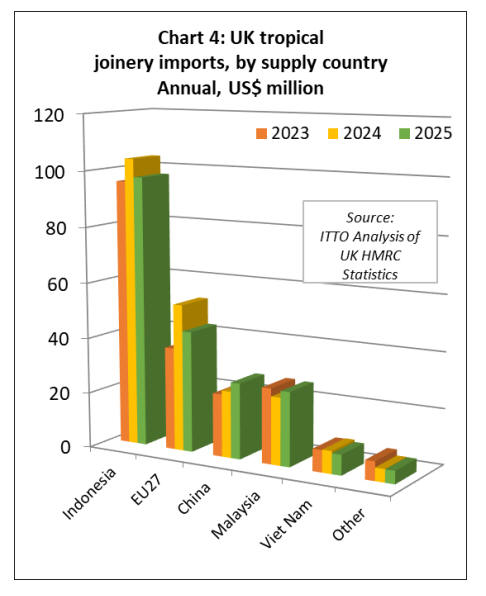

Falling UK imports of joinery products

Total UK import value of tropical joinery products

decreased 5% to US$206.8 million in 2025 while import

quantity was down 3% to 71,100 tonnes. Following a big

increase in 2024, imports of these products from the EU

fell 18% to US$43.5 million last year. Imports from

Indonesia, mainly comprising doors, were US$97.3

million in 2025, 6% less than in the previous year.

Imports also fell from Vietnam in 2025, by 10% to US$7.3

million. These declines were partly offset by rising

imports of tropical hardwood joinery products from China

(+14% to US$27.3 million), and Malaysia (+10% to

US$26.7 million) (Chart 4).

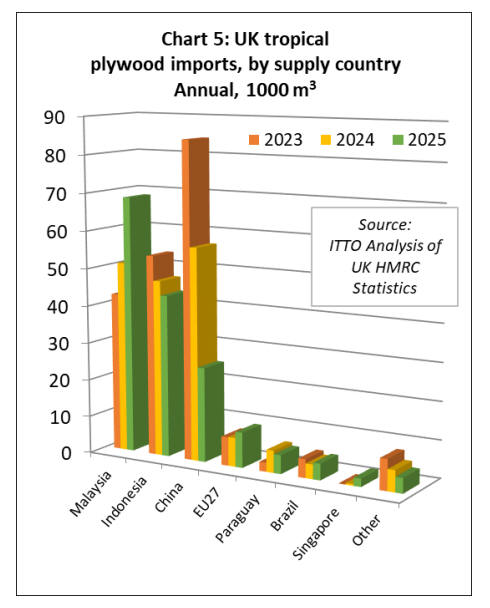

UK imports of hardwood plywood

The UK imported 162,000 cu.m of hardwood plywood

from tropical countries in 2025, 9% less than in the

previous year. Import value fell by 11% to US$100.6

million. However, this was mainly due to a decline in

imports from China.

Direct UK imports of hardwood plywood from tropical

countries increased 12% to 126,900 cu.m in 2025. Imports

were up 35% to 68,600 cu.m from Malaysia and up 13%

to 4,400 cu.m from Brazil.

Imports also increased from zero to 2,200 cu.m from

Singapore. These gains offset declines of 8% to 43,300

cu.m from Indonesia and of 16% to 5,000 cu.m from

Paraguay.

The UK imported 25,200 cu.m of plywood with an outer

layer of tropical hardwood from China in 2025, 56% less

than in 2024. In contrast, UK imports of tropical

hardwood plywood from EU countries increased last year,

by 22% to 9,400 cu.m (Chart 5).

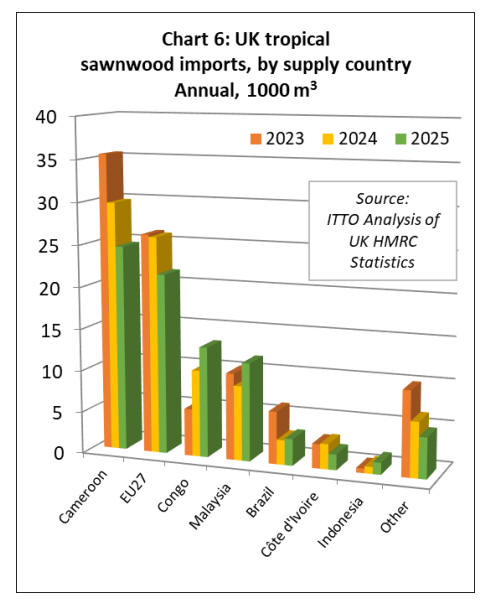

Congo and Malaysia increased share of UK tropical sawnwood

UK imports of tropical sawnwood were 82,400 cu.m in

2025, 7% less than the previous year. Import value was

down 4% to US$102.3 million. The most notable trends

last year were sharp rises in imports from the Republic of

Congo (+27% to 13,200 cu.m) and Malaysia (+31% to

11,700 cu.m).

Large percentage gains were also made in imports from

Brazil (+8% to 3,200 cu.m) and Indonesia (+72% to 1,400

cu.m). These gains offset declining imports from

Cameroon (-17% to 24,600 cu.m) and Côte d'Ivoire (-37%

to 1,875 cu.m). Indirect imports from the EU also fell, by

17% to 21,500 cu.m. (Chart 6 above).

The introduction of the log export ban and shift towards

more kiln dried production by some leading exporters in

the Republic of Congo has been particularly critical to

expansion of the UK market which has no hardwood

processing capacity of its own.

This trend also partly explains the decline in UK imports

of tropical sawnwood from the EU in 2025 as more kiln

dried product is being imported direct from the Republic

of Congo instead of being shipped first to the EU for

drying.

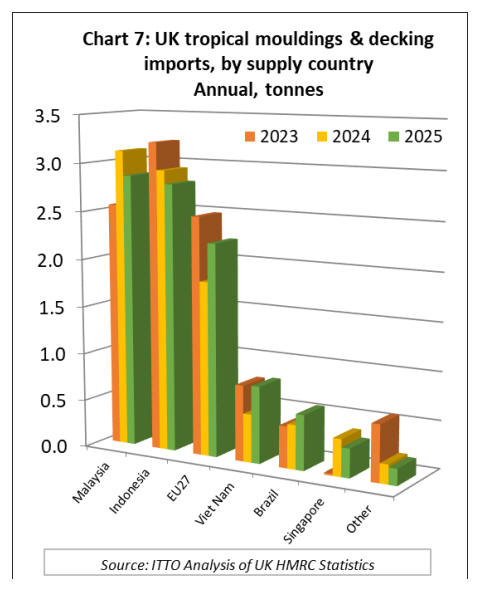

UK imports of tropical hardwood mouldings/decking

increased 3% to 9,700 tonnes in 2025. However, import

value fell 0.4% to US$26.4 million.

Import quantity declined from the two largest suppliers,

Malaysia (-8% to 2,900 tonnes) and Indonesia (-5% to

2,800 tonnes). However, imports increased from Vietnam

(+59% to 800 tonnes) and Brazil (+25% to 600 tonnes).

Imports of tropical mouldings/decking imports from the

EU also increased, by 22% to 2,200 tonnes (Chart 7).

|