The sawmill curtailments of recent months, especially those ongoing in the

western part of North America, served to bring lumber prices up slightly. At

this point, levels are still somewhat below cost-of-production in the

important supply basket of British Columbia – which has been roughly

estimated at approximately US$500 mfbm.

The strategy of reducing production, carried out in a quite disciplined way,

is mainly to prevent prices from falling even further. While building and

construction activity is relatively good for the time of year, there are a

lot of questions about what will happen with this year’s spring building

season. Will it be strong as the past two years, or muted due to the

increasing mortgage rates? It is too early to tell right now, so sawmills

continue to hedge manufacturing volumes against potentially softer 2023 new

housing starts.

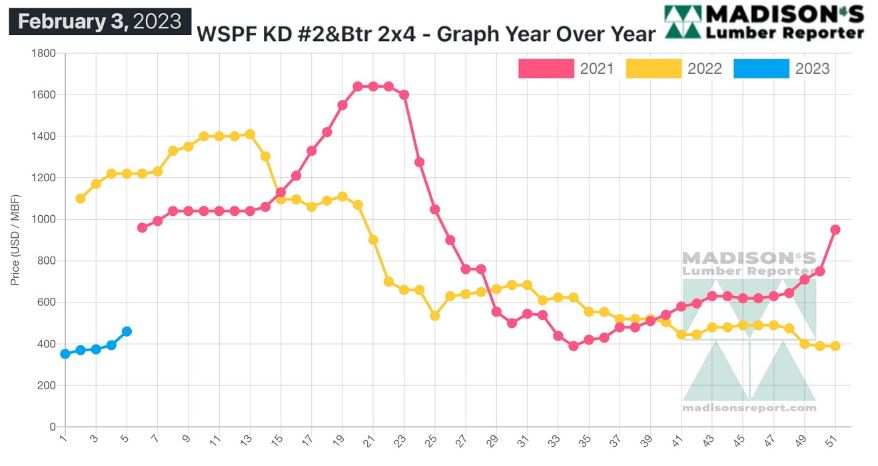

In the week ending February 3, 2023, the price of Western Spruce-Pine-Fir

2x4 #2&Btr KD (RL) was US$460 mfbm, which is up by +$66, or +17%, from the

previous week when it was $394, said weekly forest products industry price

guide newsletter Madison’s Lumber Reporter. That week’s price is up by +$88,

or +23%, from one month ago when it was $373.

Secondary suppliers reported a busier start to February than anyone could

recall in recent – or even long-term – memory.

Sales of dimension lumber and studs strengthened further while demand for

panels continued to flounder by comparison.

Prices of Western S-P-F commodities kept marching up. Frustration among

buyers was brimming, as many had avoided pulling the trigger in recent weeks

only to find themselves with further-depleted inventories amid rising

prices. With so much volume taken out of the market by curtailment and

shutdown announcements during January, sawmills easily established strong

two- to three-week order files. The sweeping operational reductions among

mills affected both lumber and studs, shifting the entire market’s

supply-demand balance heavily to the demand side.

Sales momentum of Western S-P-F continued to gather, according to suppliers

in Western Canada. Curtailment announcements made the previous week by

several major producers spurred many buyers into action as the perception of

limited supply ratcheted up. Sawmills easily established two- to four-week

order files while also boosting asking prices again. Buyers found it more

challenging to track down their needs than in recent weeks, particularly

when it came to shorter 2x4 straight lengths. Secondary suppliers reported

increased LTL business as buyers searched for coverage.

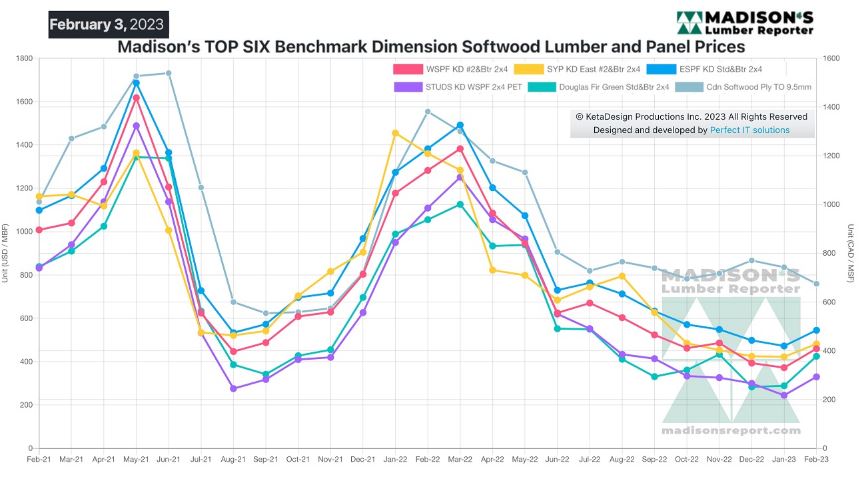

The Eastern S-P-F plywood business floundered again according to Eastern

Canadian traders. Sales activity on both sides of the border was dead quiet,

and discounted pricing appeared repeatedly. This despite mills claiming to

have order files as far out as early March, reports which were met with

skepticism by secondary suppliers. Oriented Strand Board held the line amid

weak inquiry and follow-through. Numbers were flat as Canadian producers

were able to keep enough product headed to more active US markets.

Compared to the same week last year, when it was US$1,220 mfbm, the price of

Western Spruce-Pine-Fir 2x4 #2&Btr KD (RL) for the week ending February 3,

2023 was down by -$760, or -90%. Compared to two years ago when it was $960,

that week’s price is down by -$500, or -70%.

More Reports: