As March Rolled Along The Ongoing Harsh Winter Weather Continued To Stymie

Lumber Sales.

Some prices of Southern Yellow Pine started to rise as the US south at least

started to thaw. All across North America the supply chain was a major topic

as trucks were increasingly difficult to source and freight prices rose up

to 30% compared to one year ago.

Supply of lumber remained constant while demand was more toward inquiry than

actual purchases.

Those who truly wanted wood asked for quick deliveries, which just was not

possible. The seemingly now-entrenched habit of not stocking inventory could

become a real problem in the coming weeks as spring truly arrives. While

lumber supply continues low as so many

sawmills have reduced manufacturing volumes, log yards are well stocked.

Which means, once construction activity gets going in spring, lumber

producers will be able to ramp up volumes as there is plentiful supply of

fibre.

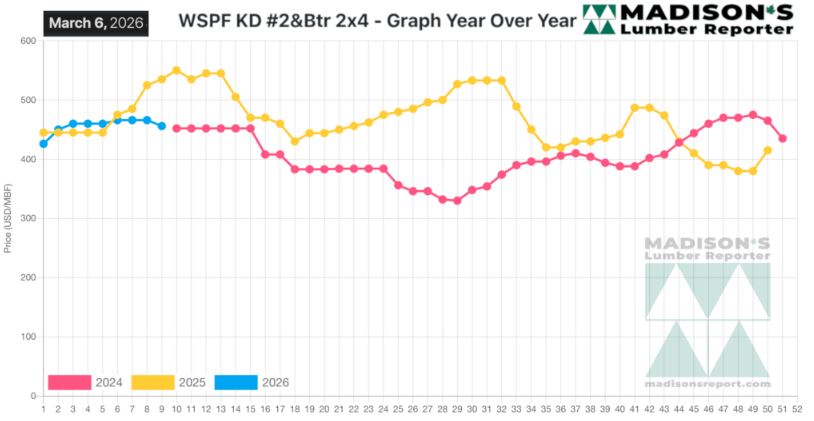

In the week ending March 6, 2026 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$456 mfbm, which was down -$10, or -2%, from the

previous week when it was $466, said weekly forest products industry price

guide newsletter Madison’s Lumber Reporter.

That week’s price was down -$9, or -2%, from one month ago when it was $465.

Compared To The Same Week Last Year, When It Was Us$535 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending March 6, 2026

Was Down -$79, Or -15%.

Compared To Two Years Ago When It Was $452, That Week’S Price Was Up +$14,

Or +3%.

There continued uncertainty in all species, categories, and grades;

lumber traders waited for the other shoe to drop before spring.

KEY TAKE-AWAYS:

Winter weather still reigned, keeping consumption quiet in many key markets

across North America.

The demand side for Western-SPF in the US appeared to be waiting on

suppliers to confirm the direction of the market.

Year-long transportation issues resulted in higher operating costs and

reduced supply of empty flatbeds.

The tone and pace of business for Western-SPF traders in Canada was largely

unchanged.

Suppliers of Eastern-SPF reported the overall direction of business remained

indeterminate.

Eastern lumber buyers were challenged by a tricky market as print levels

floated around the previous week’s levels.

Players in the US voiced their frustrations with constant issues in

trucking.

The Southern Yellow Pine market was hard to tell what direction business was

headed, with so many unanswered questions and spring rapidly approaching.

The bulk of SYP inquiry was for wood that could deliver tomorrow, which was

not possible.

The apparent 20-30 per cent higher freight rates over last year did not help

operators.

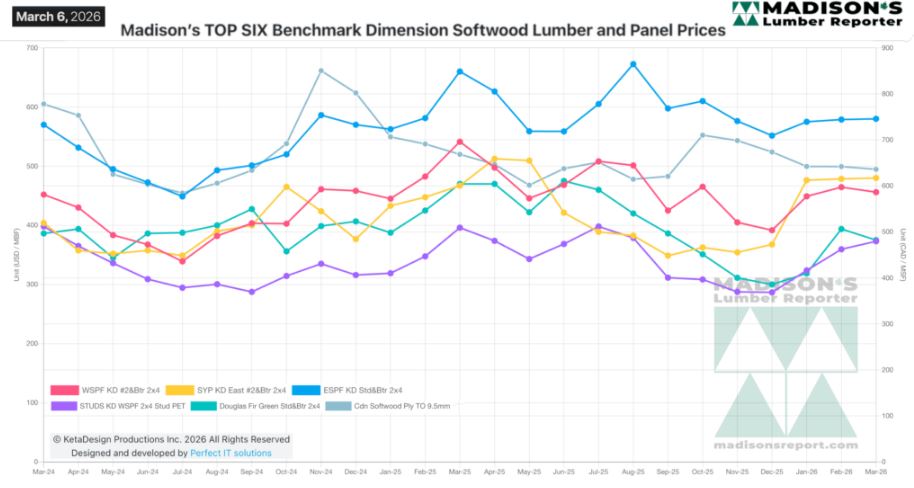

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: