As May Dawned Most Players In The North America Lumber Industry Remained

Firmly On The Side Of Caution.

While there was a welcome increase in lumber demand since April, most prices

remained flat. Sales volumes continued to be lower than was the busy spring

season historically.

Inventories of solid wood material throughout the supply chain were still

low, something that has lately become a chronic situation. Most were

reluctant to increase their inventories for fear of getting hit with higher

replacement costs.

Transportation problems abounded across the continent, with buyers and

seller alike spending more time locating their trucks and rail cars than

actually making deals. Rapidly increasing fuel costs were on the top of

everyone’s minds.

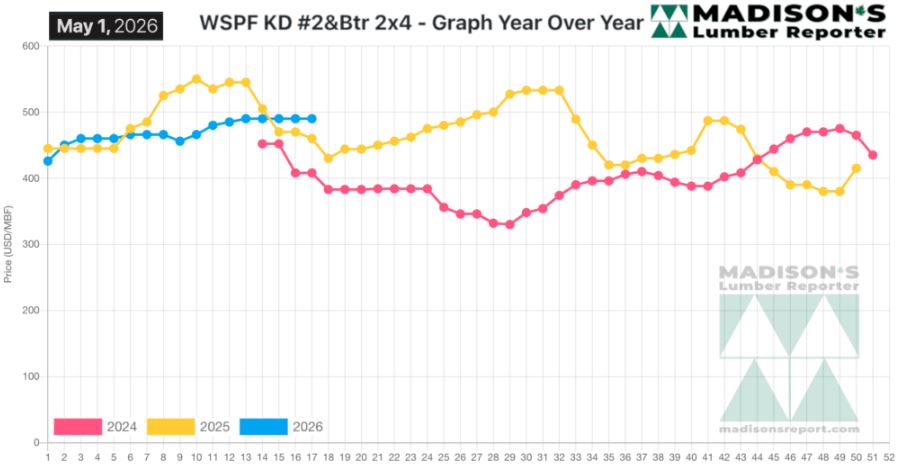

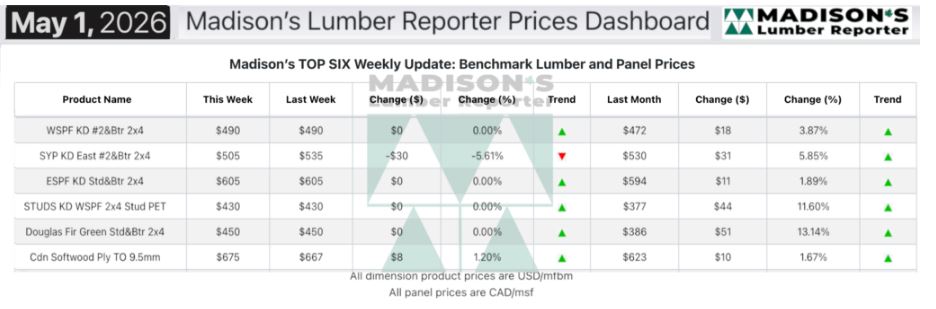

In the week ending May 1, 2026 the price of Western Spruce-Pine-Fir 2×4 #2&Btr

KD (RL) was US$490 mfbm, which was flat from the previous week, said weekly

forest products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price was flat from one month ago when it was $490.

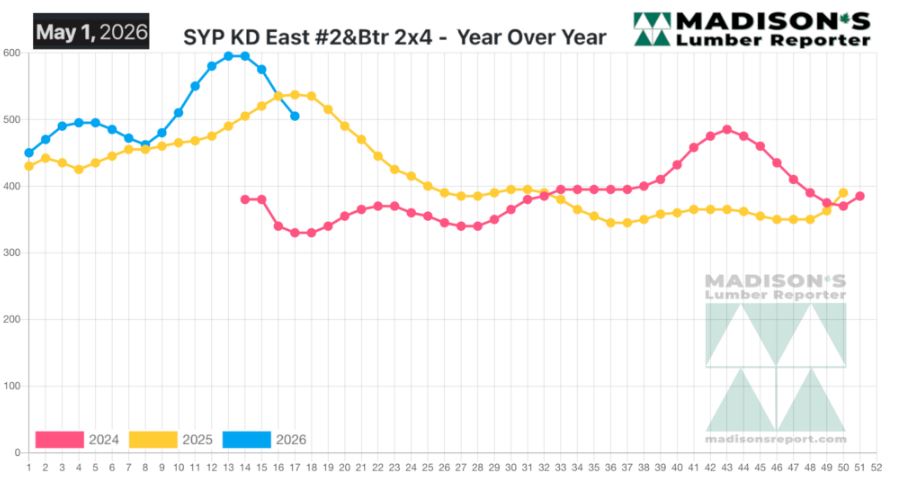

In the week ending May 1, 2026, the price of Southern Yellow Pine East Side

2×4 #2&Btr KD (RL) was US$505 mfbm. This was down -$30, or -6%, from the

previous week when it was $535.

That week’s price was down -$56, or -10%, from one month ago when it was

$561.

Compared To The Same Week Last Year, When It Was Us$460 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending May 1, 2026

Was Up +$30, Or +7%.

Compared To Two Years Ago When It Was $408, That Week’S Price Was Up +$82,

Or +20%.

Reports varied considerably between sawmills, print, and on-ground

levels amid a broad sense of unease in the market; while Southern Yellow

Pine continued its correction down.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Players of Western-SPF in the US reported precious little slack in the

system.

Purchasing continued to be on a lean, hand-to-mouth basis.

Limited overall supply and ongoing issues in transportation played havoc

with production schedules and delivery timelines.

Demand for Western-SPF in the Canada was undeniably better than at the start

of April.

Price spreads between sawmill-asking and on-the-ground grew further.

Trading volumes of Eastern-SPF were decent — though subpar for the time of

year.

Southern Yellow Pine continued trading down in a freight vacuum, while price

fragmentation and availability discrepancies increased again.

Delayed deliveries and frustrated retail customers abounded as trucking

issues dominated much of the conversation.

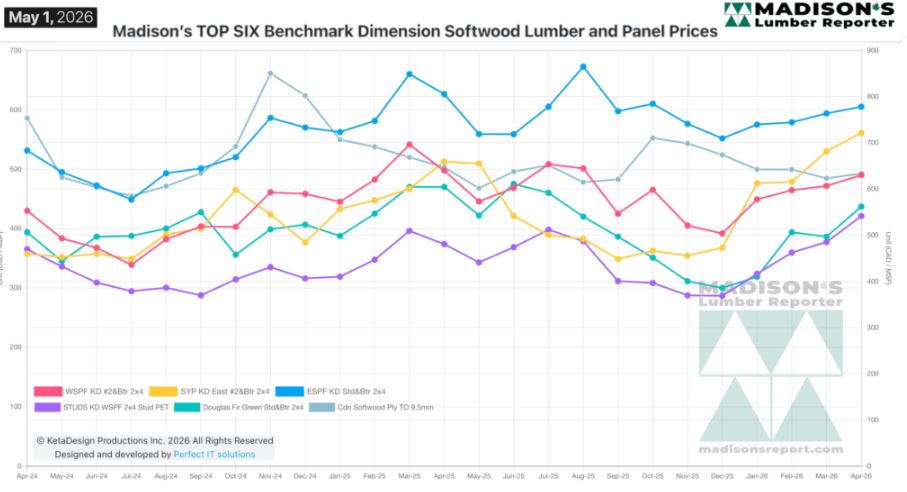

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: