North American lumber industry struggles with closures,

tariffs and post-pandemic demand shift

North American lumber producers face a multi-layered

challenge as permanent capacity closures, steeply rising

Canadian duties, and potentially transformative Section 232

tariffs converge to create what could be the most disruptive

trade environment since the Smoot-Hawley era. These shifts are

occurring while the market continues to work through

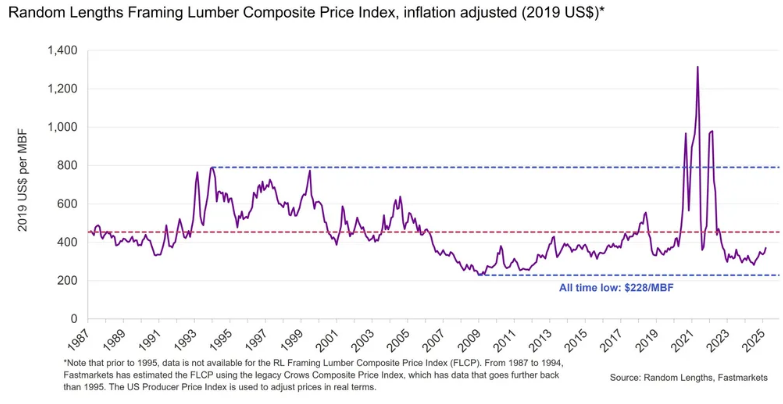

post-pandemic demand recalibration, with consumption still

approximately 9% below COVID-era peaks.

“We are dealing with a massive event that could literally cancel

out a century of tariff reductions from globalization,”

explained Dustin Jalbert, senior economist for wood products at

Fastmarkets, at the outlook presentation held on the sidelines

of the 2025 Montreal Wood Convention. “Even if the most extreme

tariff scenarios don’t materialize, the industry cost curve is

fundamentally shifting.”

A significant downside risk looms, however, if the broader

economy enters a major recession accompanied by sustained high

mortgage rates. Unlike typical downturns where housing demand

might benefit from countercyclical monetary policy easing,

retaliatory measures from China and other trading partners could

keep bond yields elevated. This worst-case scenario – combining

demand destruction with stubbornly high 30-year mortgage rates –

would compound the industry’s challenge by eliminating the

typical relief valve of lower financing costs stimulating

housing activity amid economic weakness.

Capacity rationalization: 5 BBF and counting

The North American lumber industry has undergone

unprecedented capacity rationalization, with approximately 5

billion board feet (BBF) of indefinite or permanent sawmill

closures over 2023-2024 alone. While 2023 shutdowns were

concentrated primarily in British Columbia, the 2024 closures of

3.2 BBF were more geographically dispersed, affecting operations

across BC, the Pacific Northwest, and even the traditionally

resilient U.S. South.

“This is a wipe-out year,” Jalbert noted. “I know it’s a rough

year for capacity closures when I keep having to fiddle with my

font and make it smaller and smaller to fit it all on one

slide.”

British Columbia’s production has experienced a structural

decline of nearly 50% since 2017, dropping from approximately 13

BBF to around 7 BBF annually. This collapse stems from a

confluence of factors: diminishing recoverable timber from the

mountain pine beetle epidemic, old-growth habitat protection

policies reducing Annual Allowable Cut (AAC), and the persistent

burden of U.S. countervailing and anti-dumping duties.

Perhaps most telling for market observers is that 2024 marked

the first year since 2020 that North America experienced a net

reduction in operable sawmill capacity, despite continued SYP

capacity expansion in the U.S. South. Fastmarkets projects this

net capacity decline will accelerate in 2025, with another

reduction, albeit smaller, following in 2026 as the “slow-burn

bull whip of supply adjustment” continues to work through the

system.

The triple threat: duties, Section 232 and IEEPA tariffs

The emerging “Trump Tariffs 2.0” environment introduces

multiple, potentially overlapping trade barriers that could

fundamentally alter North American supply patterns. Industry

participants must now navigate a complex web of policy measures:

Please

click here to view the complete article.

Source:

fastmarkets.com